The $2.59 Trillion AI Infrastructure Stack: A Layer-by-Layer Breakdown of Gartner's 8 Segments

Gartner forecasts $2.59 trillion in global AI spending for 2026, with infrastructure capturing 54%. But this is not a homogeneous market — it is eight distinct sectors stacked together, each with its own growth rate, barriers to entry, competitive landscape, and product roadmap. This article walks through every segment from largest to smallest: what it covers, how big it is, who leads it, what a competitive product must offer, and where the product形态 is heading.

Gartner's Defining Framework

Gartner partitions "AI spending" into eight mutually exclusive segments. The single most important principle for understanding this taxonomy: each segment's money comes from a different budget line and lands in different hands.

| Segment | 2026 Size | Share | 2025→26 Growth | 2026→27 Growth | Where the Money Goes |

|---|---|---|---|---|---|

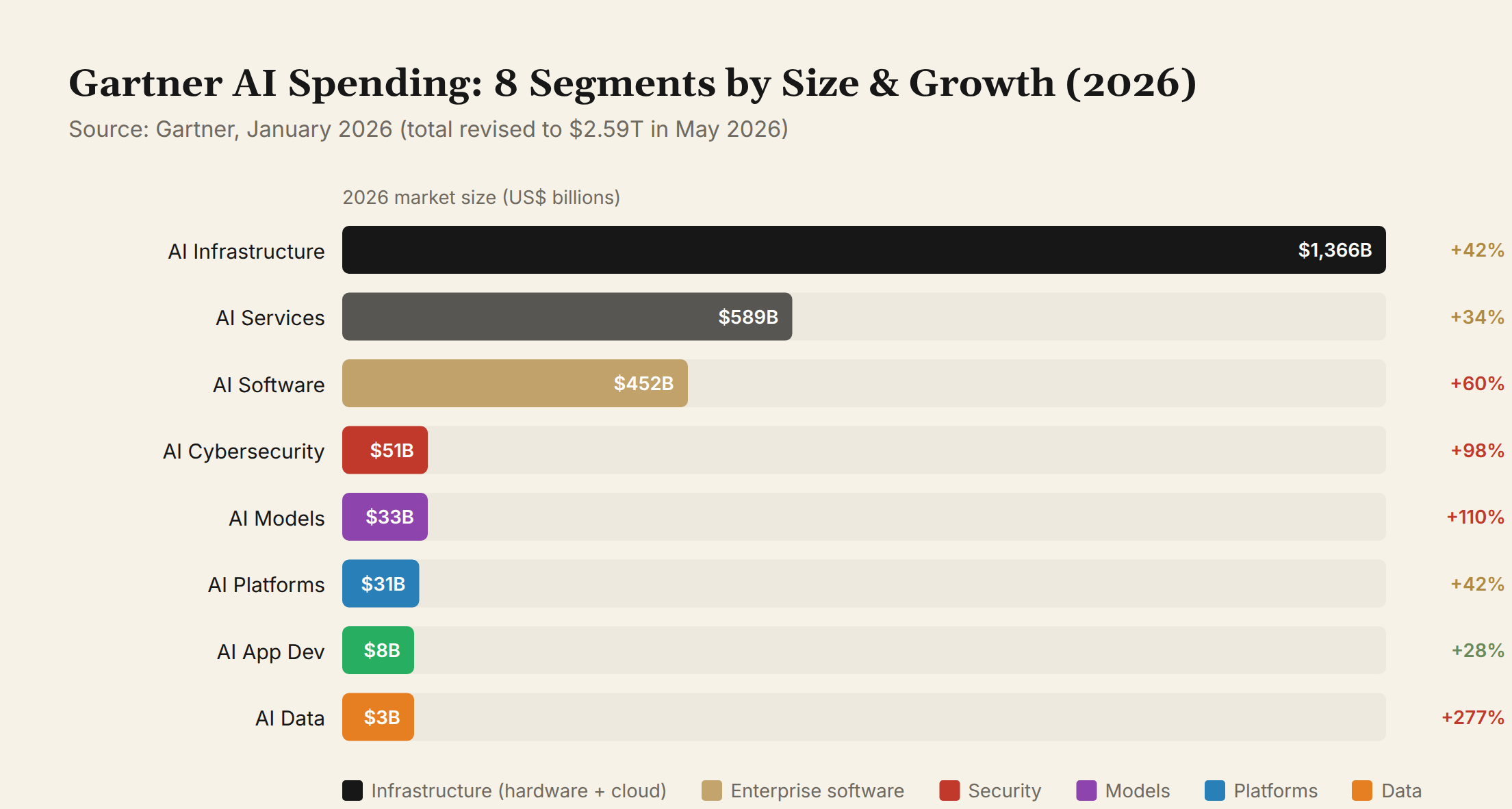

| AI Infrastructure | $1,366B | 54% | +42% | +28% | GPUs, servers, cloud, networking, power |

| AI Services | $589B | 23% | +34% | +29% | Consulting, integration, managed operations |

| AI Software | $452B | 18% | +60% | +41% | AI features embedded in CRM/ERP/productivity |

| AI Security | $51B | 2% | +98% | +68% | Securing AI systems themselves |

| AI Foundation Models | $33B | 1.3% | +110% | +65% | GPT/Claude/Gemini APIs |

| AI Platforms | $31B | 1.2% | +42% | +43% | MLOps, Agent building tools |

| AI App Development | $8.4B | 0.3% | +28% | +30% | RAG frameworks, vector databases |

| AI Data | $3.1B | 0.1% | +277% | +107% | Data labeling, synthetic data, quality |

| Total | $2,528B | 100% | +44% | +32% |

Source: Gartner detailed release, January 2026 (total $2.53T / +44%). The May revision updated the total to $2.59T / +47% and raised foundation model growth from +83% to +110%. Segment-level breakdowns were not republished with the revision; January figures remain the authoritative source for per-segment data.

Gartner also separately tracks AI Agent Software ($206.5B, a sub-category of AI Software, +139% YoY) — the fastest-growing independently metered category.

Three structural observations:

- Growth rate is inversely proportional to scale. The largest segment — infrastructure at $1,366B — is decelerating (42%→28%), while the smallest — AI Data at $3.1B — is growing fastest (277%→107%).

- Infrastructure dominates absolutely, but its share is shrinking. From 55% in 2025 to a projected 52% in 2027. Software and services are eating into its share.

- Total market growth slows from 44% to 32% in 2027. The absolute increment remains enormous (+$809B), but capital efficiency will become the focal point.

I. AI Infrastructure — $1,366B

Definition

Physical hardware and cloud infrastructure supporting AI workloads. Includes AI-optimized servers, AI processing semiconductors, AI networking, AI-optimized IaaS, and data center physical facilities. This segment is vendor-driven (NVIDIA, hyperscalers), not enterprise-ROI-driven — in Gartner's words: "vendors are building AI infrastructure faster than enterprises can digest it."

Sub-Segment Breakdown

The sub-segments below total approximately $978B. The remaining $388B is distributed across AI-optimized storage, edge AI devices, AI-optimized endpoint devices, and other hardware categories not individually broken out.

1.1 AI-Optimized Servers — $421.6B

The largest sub-segment. Gartner forecasts a 3× increase to $699.7B within five years.

| Player | Position | 2025-2026 Data | Core Products |

|---|---|---|---|

| ODM Direct (Foxconn/Wiwynn/Quanta) | Hyperscaler white-label | ~50% global server share (IDC Q1'26, down from 64% in 2025) | Custom GPU racks for AWS/Meta/Google |

| Dell | #1 OEM | ~20% AI server share, FY27 target $60B | PowerEdge XE9680/FE series, AI Factory (with NVIDIA) |

| HPE | #2 OEM, supercomputing DNA | ~15% share | ProLiant XL + Cray EX, HPE AI Factory |

| Supermicro | Top-3 OEM, shadowed by export-control investigation | ~10% share, three former executives indicted for alleged illegal AI server exports to China | 4U/8U GPU servers, liquid-cooling specialization |

| Lenovo | Fastest-growing traditional OEM | ~11% share, revenue +26% | ThinkSystem SR675/V3 |

Table stakes for a competitive product:

- Rack-level delivery (whole-cabinet, not piecemeal assembly)

- Liquid-cooling readiness (CDU integration, 100kW+/rack)

- GPU density (8-72 GPUs/rack)

- Full NVLink/NVSwitch interconnect

- Hybrid liquid-air cooling capability (transition-period requirement)

- Supply chain flexibility (multi-GPU-vendor compatibility)

Where product形态 is heading:

- Integrated liquid-cooled appliances: The industry is moving from "servers plus bolt-on CDU" to "rack-as-compute-unit," with cooling, power, and compute pre-integrated at the factory. Dell's AI Factory and HPE's Cray line are already on this path.

- Multi-chip compatibility: No longer NVIDIA-only — the same rack must support AMD MI400, Google TPU, or custom ASICs. Supermicro's legal troubles are accelerating this trend: customers do not want to be held hostage by a single GPU supplier.

- Edge AI servers: 5-20kW-class "mini AI racks" targeting enterprise campuses and inference scenarios. ABI Research forecasts edge AI servers will exceed $50B by 2030.

1.2 AI Processing Semiconductors — $289.4B

| Player | Share | 2026 Revenue | Core Products | Moat |

|---|---|---|---|---|

| NVIDIA | ~80-85% | FY26 DC $193.7B, Q1 FY27 $75.2B | Blackwell B200/GB200, Rubin R200 (next-gen) | 17 years of CUDA ecosystem accumulation |

| AMD | ~5-7% | DC GPU est. $15B (MI400 $7.2B) | MI400X/MI450 series | Price-performance + 2nm first-mover advantage |

| Google TPU | ~5-6% | Internal use, saving on NVIDIA spend | TPU v6/v7 (Trillium+) | In-house design and consumption, vertical integration |

| Amazon | ~3-5% | Trainium 2 at scale | Trainium 2/3 + Inferentia2 | Custom ASIC, cost-controllable |

| Broadcom | Custom ASIC | AI revenue $20B+ (+65%) | Custom AI chip design for Google/Meta | Unique: simultaneously in networking and silicon |

Table stakes for a competitive product:

- Compute: Training >5 PFLOPS (FP4), Inference >1000 TFLOPS (INT8)

- HBM bandwidth: >5 TB/s (HBM3E), next-gen >8 TB/s

- Interconnect bandwidth: NVLink 1.8 TB/s or equivalent

- Energy efficiency: >2 TFLOPS/W

- Software ecosystem: mature compiler, operator libraries, debugging tools

- Multi-precision support: FP4/FP8/INT8/BF16

Where product形态 is heading:

- Inference-specific silicon rises: Inference will account for 70-80% of AI compute by 2028-2030. Inference does not require training-grade precision or interconnect, opening space for low-cost ASICs. NVIDIA's Cyber (inference-specialized) and AMD's Instinct MI420 series are both moving in this direction.

- Chiplet + 3D stacking becomes standard: CoWoS packaging capacity limits are forcing manufacturers toward chiplet partitioning. Blackwell is already dual-die; Rubin may go quad-die. But packaging yield and warpage management (the root cause of Kyber delays) represent a new battleground.

- Optical interconnect chips: Ayar Labs, Lightmatter, and others are developing silicon photonics integrated circuits, upgrading I/O from electrical to optical signals to break through the bandwidth wall. Data center entry expected 2027-2028.

1.3 AI Networking — $28.7B

| Player | 2026 Revenue | Core Products | Position |

|---|---|---|---|

| NVIDIA (Mellanox) | FY26 Q4 networking $11B (+263%) | NVLink/NVSwitch, Spectrum-X Ethernet, BlueField DPU | Bundled with GPU shipments; networking growing faster than GPUs |

| Broadcom | AI semiconductor quarterly $8.4B→$10.7B | Tomahawk 6 (100Tbps AI switch), custom ASIC | The only company simultaneously in networking and silicon |

| Arista | Revenue guidance ~$3.25B | AI data center Ethernet switches | Primary Meta/Microsoft AI networking supplier |

| Cisco | Network revenue ~$15B | Silicon One unified architecture | Enterprise AI networking |

| Marvell | Custom chip growth | Custom switching ASIC, DSP | Cloud-vendor-customized networking silicon |

Table stakes for a competitive product:

- Bandwidth: 400G→800G→1.6T port speed evolution

- Microsecond-level latency (AI training is acutely latency-sensitive for collective operations)

- Large-scale non-blocking: 10,000+ GPU full interconnect, oversubscription = 0

- Congestion control: RoCE/DCQCN or equivalent

- Observability: per-flow monitoring, automated diagnostics

- Compute-layer coordination: topology-aware scheduling

Where product形态 is heading:

- CPO (Co-Packaged Optics): Integrating optical transceivers into the switch chip package, cutting power consumption 50% and tripling port density. Broadcom has demonstrated this in Tomahawk 5, but volume production is still 2027-2028.

- Non-linear topologies (RNG/flat networks): AWS's Random Network Graph breaks the limitations of traditional Clos topology, reducing network cost by 40%. Expect more cloud providers to follow.

- Network as GPU programming interface: NVLink C2C (chip-to-chip) makes multiple GPUs appear as a single massive GPU in software. This abstraction will extend to rack-level by 2027 — an entire rack that "looks like one GPU."

1.4 AI-Optimized IaaS — $38.3B (CAGR 71%, fastest-growing within infrastructure)

| Player | Share | 2026 AI Cloud Revenue | Core Products |

|---|---|---|---|

| AWS | ~30% | Bedrock + EC2 P5/G7 | Broadest model selection + largest GPU capacity |

| Azure | ~22% | OpenAI exclusive + ND H100/H200 | Enterprise entry-point advantage |

| GCP | ~13% | Vertex AI + TPU | TPU cost advantage |

| Oracle Cloud | ~8% | OCI GPU + OpenAI partnership | Price competitiveness + government/enterprise relationships |

| CoreWeave | ~5% | 2025 $5.13B → 2026 guidance $12-13B | Fastest cloud to reach $5B annual revenue (2025); pure GPU cloud |

Table stakes for a competitive product:

- GPU multi-tenant isolation (security + performance guarantees)

- Elastic scheduling (second-level scale-up/down)

- One-click multi-model deployment (vLLM/SGLang/TensorRT-LLM built-in)

- Cross-region low-latency inference (edge nodes)

- Cost transparency (fine-grained per-token or per-GPU-second billing)

- Managed fine-tuning (LoRA/SFT/RLHF platformized)

Where product形态 is heading:

- Inference-as-a-Service standardization: Users will not select GPU models — they will declare SLAs (latency, throughput, availability), and the cloud will automatically choose the optimal model+hardware combination. AWS Bedrock's Provisioned Throughput is already on this path.

- GPU futures market: CoreWeave is already writing long-term GPU reservation contracts. When GPU supply tightens, inter-cloud GPU capacity trading will become routine.

- Private GPU cloud rise: Enterprises do not want to be held hostage by hyperscaler pricing. Private AI Cloud (enterprise-owned GPU clusters with managed operations) is emerging as a third option.

1.5 Data Center Physical Infrastructure — ~$200B+

| Player | Core Products | Position |

|---|---|---|

| Vertiv | Liquid-cooling CDU, thermal management, power distribution | AI data center cooling leader |

| Eaton | Electrical management, UPS | Power distribution + energy management |

| Schneider Electric (incl. APC) | UPS, PDU, cooling, DCIM | Full-stack physical infrastructure |

| Vicor | High-density power modules | The "last mile" of GPU power delivery |

| ABB | Medium/low-voltage distribution, transformers | End-to-end power chain from grid entry to rack |

Table stakes for a competitive product:

- Liquid-cooling readiness (cold-plate/immersion, modular CDU)

- High-voltage DC power distribution (800V DC)

- PUE < 1.2 design capability

- Modularity (factory-prefabricated, rapid on-site deployment)

- Intelligent energy management (AI-scheduled load balancing)

Where product形态 is heading:

- AI data center as product: Factory-prefabricated "AI data center modules" — shipping-container-sized units with cooling, power, networking, and GPU servers pre-installed. Arrive on site, connect power and water, start computing. Dell, HPE, and Supermicro are all building these.

- Power becomes the #1 siting criterion: Not bandwidth, not latency — but "is there enough electricity?" JLL forecasts that U.S. data center construction over the next 5 years will hit $70B/quarter, constrained not by GPU supply but by power availability.

- Liquid cooling shifts from optional to standard: At 100kW+/rack density, air cooling is physically impossible. By 2027, liquid-cooling penetration in new AI data centers will approach 100%.

II. AI Services — $589B

Definition

Professional services that help enterprises plan, implement, and operate AI systems. Includes strategy consulting, system integration, and managed operations. The bottleneck here is not technology — it is talent supply.

Leading Players

| Player | Position | AI-Related Revenue | Core Products |

|---|---|---|---|

| Accenture | World's largest AI integrator | GenAI bookings $5.9B (FY25), AI-related revenue growing rapidly | AI Refinery (with NVIDIA), data pipeline construction, ERP AI-ification |

| McKinsey (QuantumBlack) | High-end strategy consulting | AI project revenue $5B+ | AI strategy planning, use-case identification, organizational change |

| Deloitte | Audit + consulting dual engine | AI business ~$15B | Generative AI Practice (30,000+ consultants) |

| IBM | Hybrid cloud + AI | Software revenue ~$12B (incl. watsonx) | watsonx platform + consulting + managed services |

| TCS/Infosys/Wipro | Offshore delivery | AI projects growing rapidly | AI talent outsourcing, model operations, data labeling management |

Table stakes for a competitive offering:

- Industry-specific model library (pre-built solutions for finance/manufacturing/retail)

- Standardized pilot-to-production methodology

- Data governance and compliance framework (EU AI Act, industry regulation)

- Change management (workforce training, process redesign)

- ROI measurement system

Where product形态 is heading:

- AI services themselves get replaced by AI: Consulting firms are already using AI for initial analysis and report generation; revenue per consultant will jump. But Gartner predicts that by 2028-2029, autonomous business will be a "net positive job creator" — new work categories will outnumber those displaced.

- Productized consulting: The shift from "selling hours" to "selling AI processes." Accenture's AI Refinery is packaging consulting methodology into software.

- AI FinOps consulting: Helping enterprises audit and optimize token spend — an entirely new category, corresponding to the "Establish AI FinOps" recommendation in our companion article.

III. AI Software — $452B

Definition

Enterprise application software with built-in AI capabilities. Finished products for end-users — CRM, ERP, productivity suites, customer service. Not developer tools.

Note: AI Agent Software ($206.5B) is a sub-category of AI Software, not a standalone segment.

Leading Players

| Player | AI Revenue | Core Products | Position |

|---|---|---|---|

| Microsoft | M365 Copilot ~$5B+ ARR | 365 Copilot, GitHub Copilot, Dynamics 365 Copilot | AI features permeating every product line |

| Salesforce | Agentforce ~$2B+ ARR | Agentforce, Einstein GPT, Data Cloud | Enterprise Agent #1 brand |

| ServiceNow | Now Assist ARR ~$500M+ | Now Assist, Agentic AI for IT/HR/CSM | Strongest workflow + AI integration |

| Workspace Gemini | Gemini for Workspace | Multimodal + search integration | |

| Oracle/SAP | Embedded AI | Oracle Fusion AI, SAP Joule | AI-ifying the ERP/CRM installed base |

| Cursor | ARR $1B (doubled in 5 months) | AI-native code editor | Revenue per employee $6.1M; Fortune 500 penetration |

Table stakes for a competitive product:

- AI-native architecture (not "adding AI features" but "designed around AI")

- Natural language as the primary interface

- Multi-Agent collaboration (different Agents handling different sub-tasks)

- Enterprise data security (data never leaves tenant boundary)

- Auditability (full Agent decision-chain logging)

- Configurable autonomy levels (human-in-the-loop vs. fully autonomous)

Where product形态 is heading:

- From "AI features" to "AI employees": Salesforce Agentforce already lets enterprises "hire" AI Agents to handle complete business processes (customer service, sales leads, scheduling). The next step: AI Agents with their own "job descriptions," "KPIs," and "managers."

- $234B at risk of replacement: Gartner predicts $234B of enterprise application software spending faces displacement by Agentic AI. SaaS products surviving on feature-stuffing are the most vulnerable — an Agent does not need 100 feature pages, just one API.

- Pricing model revolution: per-seat replaced by per-task/per-outcome. Salesforce is already experimenting with per-conversation pricing.

IV. AI Security — $51B

Definition

Tools that protect AI systems themselves. This is not "using AI for security" (that would be AI-enhanced traditional security) — it is defense against AI-specific threats: prompt injection, model extraction, data poisoning, Agent privilege escalation.

Leading Players

| Player | Market Cap / Valuation | 2026 Revenue/ARR | Core Products |

|---|---|---|---|

| Palo Alto Networks | ~$128B | FY26 ~$11.4B (+31%) | Cortex AI, Prisma Cloud AI Security, XSIAM |

| CrowdStrike | ~$100B | ARR $5.5B (+24%) | Falcon Platform + Agentic MDR |

| Microsoft | — | Not broken out | Defender for AI, Purview, AI Security Score |

| Zscaler | ~$35B | ARR ~$2.2B | Zero Trust + AI data security |

| Fortinet | ~$80B | Revenue +15% | FortiAI, network security + AI threat detection |

| Wiz | Acquired by Google for $32B | ARR ~$700M | Cloud-native security, AI workload protection |

Table stakes for a competitive product:

- Prompt injection detection and blocking

- Agent behavior auditing (full autonomous decision-chain logging)

- Model output filtering (hallucination/toxicity/compliance)

- Training data integrity verification (anti-poisoning)

- AI supply chain security (model/dataset provenance verification)

- Real-time threat intelligence (AI-specific attack pattern library)

- Compliance reporting (EU AI Act, NIST AI RMF)

Where product形态 is heading:

- AI SOC (Security Operations Center): Traditional SOCs monitor networks and endpoints; AI SOCs monitor model behavior, Agent decisions, and token traffic. This is an entirely new category — no vendor currently offers a complete solution.

- AI Red Teaming as a Service: Automated adversarial testing of client AI systems (prompt injection, jailbreaks, data exfiltration), standardized like penetration testing.

- Agent identity management: When an enterprise runs hundreds of AI Agents, "who authorized this Agent to take this action" becomes a core question. Think IAM, but for Agents — AI Identity and Access Management (AIAM).

V. AI Foundation Models — $33B

Definition

Foundation model API and licensing revenue. This is the "raw material" layer of the entire AI ecosystem.

Leading Players

| Player | Enterprise LLM Share | 2026 ARR | Core Products | Moat |

|---|---|---|---|---|

| Anthropic | 40% (2025) | ~$47B | Claude Opus/Sonnet/Haiku, Claude Code | Strongest in coding; high enterprise trust |

| OpenAI | 27% (↓from 50%) | ~$25-35B | GPT-5/o3, Sora, API | First-mover advantage, consumer brand |

| 21% | Not broken out | Gemini 3 Ultra/Pro/Flash | Multimodal + search + TPU vertical integration | |

| Meta | Open-source ($0 direct revenue) | — | Llama 4 series | Open-source ecosystem, indirect ad monetization |

| Mistral/Cohere/DeepSeek | <5% combined | $100M-$500M | Each with differentiation | European/enterprise privacy/China |

Table stakes for a competitive product:

- Reasoning capability (multi-step reasoning, tool use, long-chain tasks)

- Context window (128K-2M tokens)

- Multimodality (text + image + audio + video)

- Inference speed (TTFT < 500ms, TPS > 100)

- Fine-tuning capability (managed SFT/RLHF/LoRA)

- Enterprise security (data not used for training, private deployment)

- Pricing competitiveness ($/million tokens)

Where product形态 is heading:

- Model as component: Enterprises will no longer "pick a model." Instead, a routing layer (OpenRouter, Portkey) will dynamically select models based on task difficulty, cost, and latency. "Easy tasks to Flash, complex reasoning to Opus" will become the default configuration.

- Proprietary model commoditization: Large enterprises will demand proprietary models trained on their own data (via LoRA and similar techniques), with costs approaching open-source base model + fine-tuning fees. Model vendor revenue will shift from "general API" to "fine-tuning + hosting + inference optimization."

- Open-source catches up to closed-source: The gap between Llama/Qwen/DeepSeek and frontier closed models is closing. When open-source models reach GPT-4.5-class performance (possibly 2027), the foundation model market will face a price collapse. Long-term, model-layer profit margins are unsustainable.

VI. AI Platforms — $31B

Definition

AI/ML development and orchestration tools for developer and data science teams. MLOps, Agent building platforms, observability, DSML platforms.

Sub-Categories and Leading Players

| Sub-Category | Size | #1 | #2 | #3 | Required Capabilities |

|---|---|---|---|---|---|

| xOps (MLOps/DataOps) | $15B | Databricks ($6.9B ARR) | Snowflake (Cortex AI) | SageMaker | Experiment tracking, model registry, pipeline orchestration, versioning |

| Agent Building Platforms | $5B | LangChain (LangGraph) | CrewAI | Microsoft AutoGen | Multi-Agent orchestration, tool registration, memory/state, security sandbox |

| AI Observability | $1.3B | Arize Phoenix | Langfuse (open-source) | Helicone | Token-level tracing, cost attribution, hallucination detection, evals |

| DSML Platforms | ~$10B | Databricks | Vertex AI | Azure ML | Data prep → training → deployment → monitoring, end-to-end |

Core tension: Open-source dominates. vLLM, MLflow, and LangChain core are all free. Commercialization relies on enterprise value-adds (security, compliance, multi-tenancy, managed hosting). The biggest risk for the platform category is being "swallowed by model capabilities" — the evaluation/monitoring/orchestration features you build today may be built into the next model version.

Where product形态 is heading:

- AI FinOps platforms: Helping enterprises track "which team spent how many tokens, which Agent consumes the most, which model delivers the highest ROI." This category barely exists today, but demand has already exploded (Uber burned through its budget in 4 months).

- Eval platform standardization: Model evaluation is moving from "manual quality judgment" toward automated benchmark testing + production A/B testing + Agent behavior auditing. Langfuse and Arize are on this path.

- Agent OS: Not just building Agents, but providing a runtime for them (compute scheduling, memory management, permission control, tool marketplace) — like a smartphone operating system, but for AI Agents.

VII. AI Application Development — $8.4B

Definition

Frameworks and toolchains for building AI-native applications. Closer to the application layer than "platforms" — RAG pipelines, multimodal processing, frontend integration.

Leading Players

| Player | Position | Core Products |

|---|---|---|

| LangChain | Largest Agent/RAG framework ecosystem | LangGraph, LangSmith |

| LlamaIndex | RAG specialization | Data connectors + retrieval + reranking |

| Vercel | Frontend AI applications | AI SDK, v0 (AI UI generation) |

| Streamlit/Gradio | Prototyping | Rapid Python UI |

Table stakes for a competitive product:

- RAG pipeline (vector database + retrieval + reranking, integrated)

- Multi-model routing (automatic model selection by task/cost/latency)

- Agent workflow orchestration (conditional branching, parallelism, human-in-the-loop)

- Evaluation framework (automated + manual evaluation)

- One-click deployment (dev→prod seamless)

The slowest-growing segment (+28%), indicating that the tooling layer faces the greatest commercialization challenge under open-source pressure.

VIII. AI Data — $3.1B

Definition

Data technologies designed specifically for AI workloads. The highest growth rate (+277%), the smallest scale.

Leading Players

| Player | Position | 2026 ARR | Core Products |

|---|---|---|---|

| Scale AI | Data labeling leader | $1B+ | RLHF labeling, evaluation datasets, Data Engine |

| Databricks | Data lake + vector search | Included in $6.9B ARR | Lakehouse, vector search, feature store |

| Pinecone | Vector database | ~$100M | Cloud-native vector DB |

| Weaviate | Open-source vector DB | ~$50M | Hybrid search (vector + keyword) |

| Gretel | Synthetic data | ~$50M | Privacy-preserving data generation |

| Snorkel AI | Programmatic labeling | ~$50M | Weak supervision, data pipeline automation |

Table stakes for a competitive product:

- Billion-scale vector millisecond query (vector databases)

- Multimodal labeling (text + image + audio + video)

- Synthetic data generation (privacy-preserving, long-tail scenarios)

- Data quality monitoring (distribution drift, labeling consistency)

- Data version management (reproducible training)

- Seamless integration with training pipelines

Where product形态 is heading:

- Data becomes the model moat: When model capabilities commoditize (open-source catches up to closed-source), differentiation comes from training data. Exclusive datasets = exclusive model capabilities. Scale AI is already upgrading from "labeling service" to "data platform."

- Synthetic data at scale: When real human data is exhausted (the internet has been scraped clean), synthetic data becomes the primary source of training material. Gretel and Scale are both pursuing this. But the "model collapse" risk of synthetic data remains unresolved.

- Data valuation market: Enterprises are starting to quantify "how much is our data worth" — not in accounting-cost terms, but as strategic value: "how good a model can this data produce?"

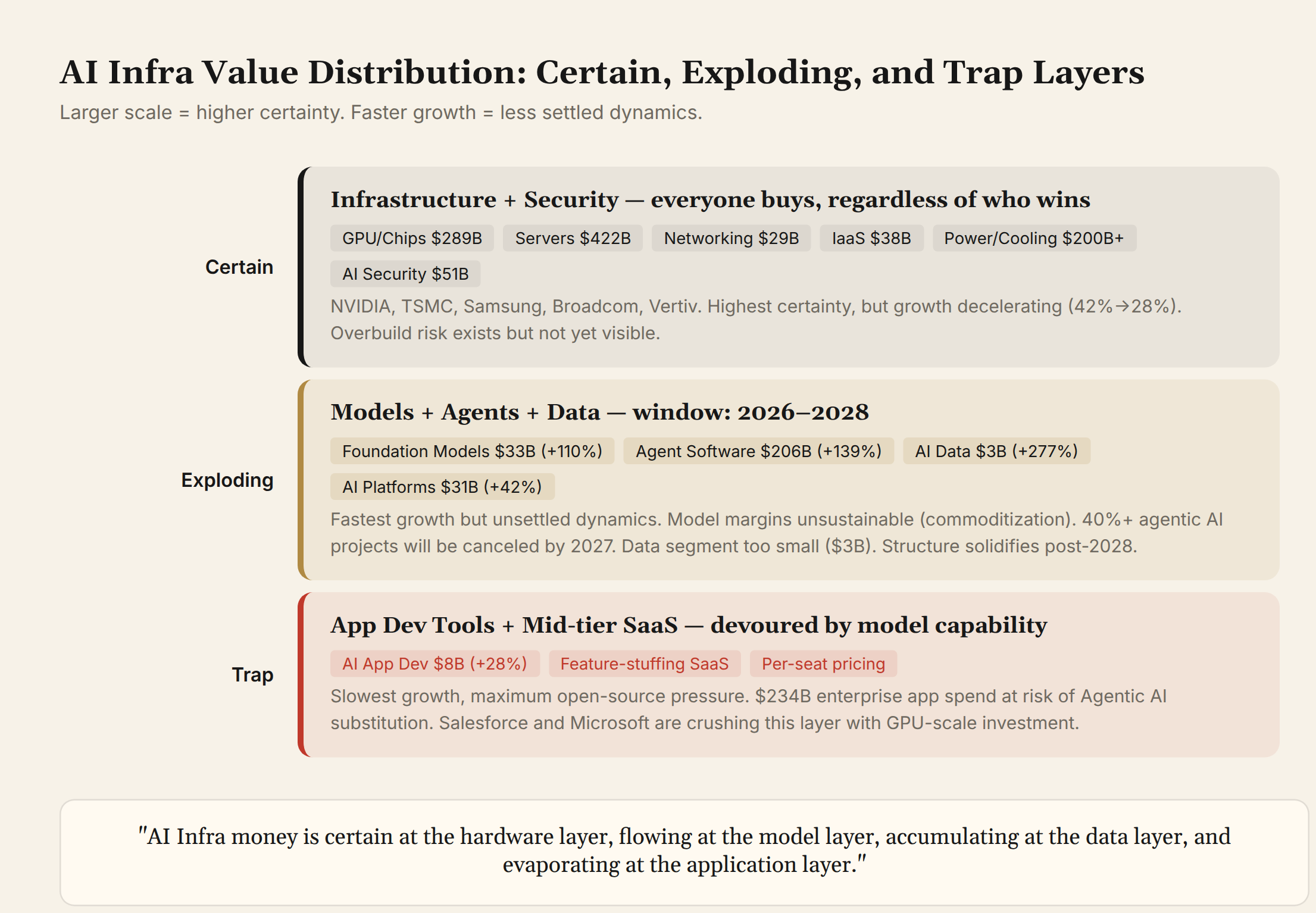

Epilogue: Three Layers of Opportunity, One Layer of Trap

Compressing the eight segments back into an investment / startup / strategy lens, the conclusion is sharp:

The certainty layer (Infrastructure + Security): The people selling shovels always profit. GPUs, HBM, networking, power, cooling — these are the highest-certainty categories. Security is "AI's insurance policy" — 98% growth signals that anxiety is converting into budget. Both categories share a defining trait: "no matter who wins, you have to buy."

The explosion layer (Models + Agents + Data): The fastest growth, but the landscape is unsettled. Model-layer margins are long-term unsustainable (commoditization). Agent software faces the risk of 40%+ project cancellation. The data layer is too small ($3.1B). The window for these three categories is 2026-2028 — after that, the landscape will harden.

The trap layer (App Development + mid-tier SaaS): Slowest growth, greatest open-source pressure, highest risk of being swallowed by model capabilities. If someone invites you to build an "AI-native CRM," now is not the right time — Salesforce and Microsoft are already using GPU scale to crush this layer.

One sentence summary: AI Infra money is certain at the hardware layer, flowing at the model layer, accumulating at the data layer, and evaporating at the application layer.