Anthropic's compute bill runs about $2M per employee per year — 4× average compensation. Uber burned through its annual AI budget in four months. Microsoft killed Claude Code licenses across an entire division. GitHub Copilot switched to usage-based billing. Three signals, one story: tokens are no longer just a billing unit. They are becoming a new form of commercial rent.

Frontier Companies Have Already Crossed the Line

Anthropic has roughly 5,000 employees and will spend about $10 billion on inference and training in 2026. That works out to $2 million in compute per employee per year, against all-in compensation of about $500,000. Compute spend is 4× payroll.

Tomasz Tunguz (Theory Ventures) used a different lens — inference costs only, engineers only — and arrived at 2.3×. Either way, the conclusion is the same: for frontier AI companies, compute is no longer a cost line item. It has surpassed headcount as the largest single expense.

These companies' revenue structures are equally extreme. Anthropic's annualized revenue reached approximately $47 billion as of May 2026 (Sacra estimate), or about $9.4M per employee. OpenAI comes in at roughly $5.5–7.8M per employee. Both rank among the highest revenue-per-employee figures in the Forbes Global 2000. Extreme cost structures, extreme revenue structures — but these two are not anomalies. They are previews: when the AI bill catches the payroll, you may need unit economics like these to survive.

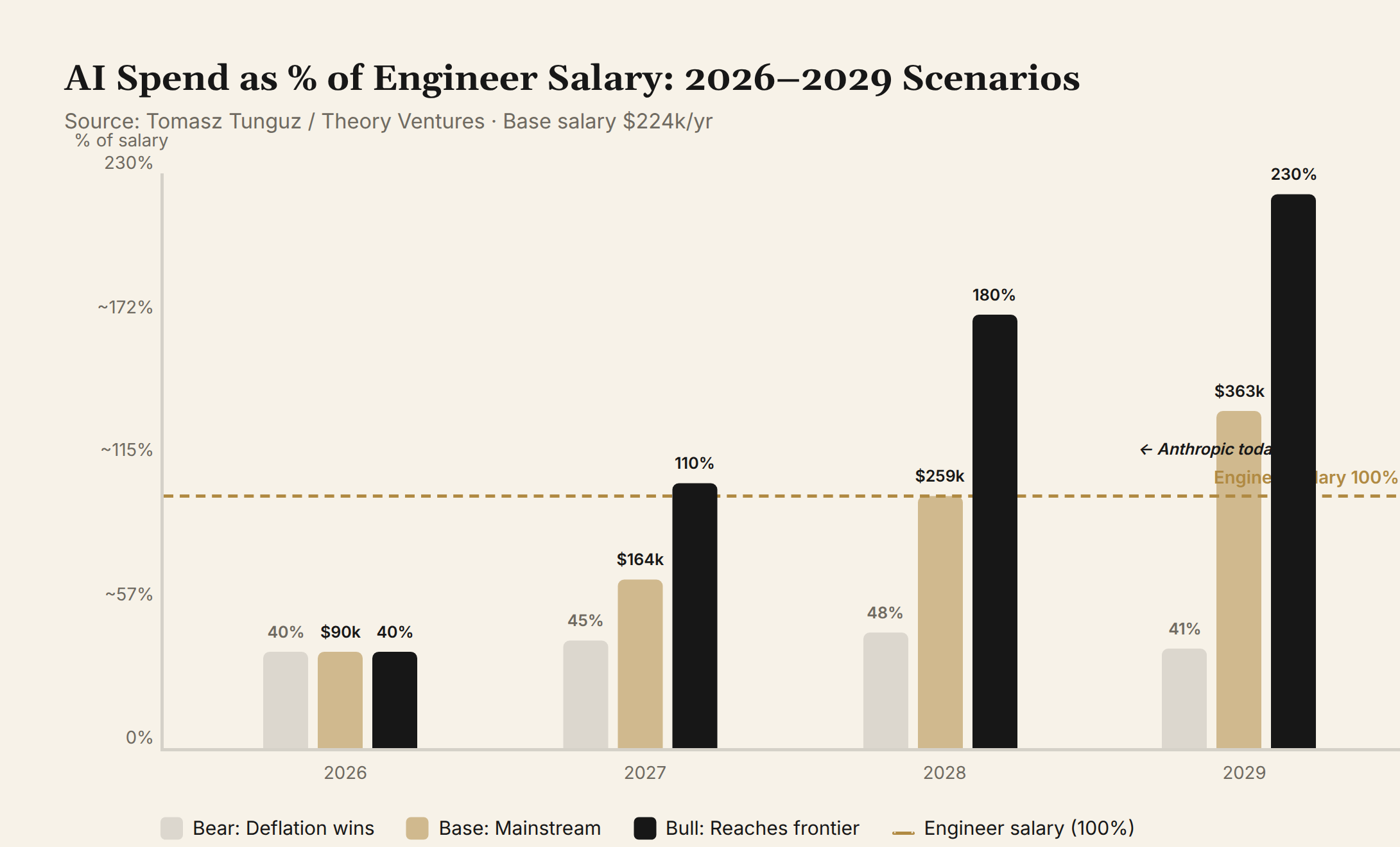

Tunguz sketched three paths to 2029 based on AI spending as a percentage of engineer salary:

| Year | Bear (Deflation Wins) | Base (Mainstream) | Bull (Reaches Anthropic) |

|---|---|---|---|

| 2026 | $90k / 40% | $90k / 40% | $90k / 40% |

| 2027 | $106k / 45% | $164k / 70% | $258k / 110% |

| 2028 | $118k / 48% | $259k / 105% | $444k / 180% |

| 2029 | $106k / 41% | $363k / 140% | $596k / 230% |

Source: Tomasz Tunguz, "When AI Costs More Than the Engineer," June 29, 2026, Theory Ventures. Base salary assumption: $224k/year.

In the Base case, the AI bill per engineer reaches 140% of salary by 2029. In the Bull case, it matches the entire revenue contribution of a median SaaS company employee.

The starting point for these scenarios is current reality. Tunguz surveyed top-tier SaaS companies: the top 1% spend $89,000 per engineer per year on AI (40% of salary), the median just $137. The gap between the frontier (Anthropic's 230%) and the mainstream (median's 0.06%) is the distance the three paths will attempt to close over the next three years.

Token's Jevons Paradox

Over the past three years, per-token inference costs have dropped by roughly two orders of magnitude. In 2023, GPT-4 32K API pricing was about $60 per million input tokens; in 2026, equivalent performance is available from open-source models for under $1 per million tokens.

But total enterprise spending hasn't gone down. It has exploded.

Three drivers compound on top of each other:

Agents replace single-shot calls. An AI coding task is not one API request — it is an autonomous decision chain: read code, analyze dependencies, generate a plan, test, verify, self-correct. Claude Code routinely consumes hundreds of thousands of tokens per task. When 84% of Uber's engineers became active AI coding agent users, monthly bills went from "negligible" to "CFO headache."

Context window inflation. From 8K to 200K to 2M tokens — a 250× increase in per-request consumption. Larger context means better results, and also means every call costs proportionally more.

Penetration is still accelerating. Most enterprises have only just moved AI coding tools from "experimental budget" to "formal line item." GitHub Copilot's shift to usage-based billing in June 2026 ($0.04/request) marks the end of the per-seat model in AI tooling — real usage variance is too large for flat pricing to work.

This is the classic Jevons Paradox: technological progress lowers unit costs, but total consumption rises instead. The cheaper tokens get, the more we use.

The Real World Is Screaming

Signals aren't only coming from frontier labs.

Uber: Deployed Claude Code + Cursor to about 5,000 engineers in December 2025. Heavy users cost $2,000/month each. The entire 2026 AI tooling budget was exhausted by April — less than four months.

Microsoft: The Experiences + Devices division announced it would cancel all Claude Code licenses by June 30, steering thousands of engineers toward its own GitHub Copilot CLI. Not because "AI doesn't work," but because costs were unsustainable.

GitHub itself: Copilot's shift to usage-based billing wasn't a product decision — it was a survival decision. Under the flat-fee model, 5% of power users consumed 100% of the margin.

The common thread across all three: when AI tools shift from assistant to primary productivity engine, usage spirals are inevitable. The problem isn't that tokens are expensive. The problem is that engineers have zero visibility into how many they're burning.

AI's "E-Commerce Moment"

The underlying logic of e-commerce's assault on physical retail was this: a new cost structure emerged that rewrote the threshold for survival. Brick-and-mortar rent, inventory, and labor were fixed costs; e-commerce used logistics and data to push marginal costs to near-zero. The result — platform giants (Amazon, Taobao) captured most transaction volume, new species (DTC brands, livestream commerce, Shopify ecosystem) emerged, and the middle layer (department stores, regional chains, mom-and-pop shops) was hollowed out.

AI is doing the same thing. "Rent" has become token cost.

| E-Commerce Era | AI Era | Underlying Logic |

|---|---|---|

| Store rent zeroed out | Server cost replaced by token cost | Cost structure substitution |

| Amazon platform | OpenAI/Anthropic API | Platform controls core capability & distribution |

| Department stores collapse | Mid-tier SaaS crushed | Middle layer loses reason to exist |

| DTC brand explosion | AI-native app explosion | New species emerge |

| Shopify empowers small sellers | Open-source models empower small teams | Entry barrier lowered |

| Luxury brick-and-mortar appreciates | Human expert services appreciate | "Non-AI" becomes scarce |

| Logistics/payments become infrastructure | GPU/cloud/power become infrastructure | Infrastructure layer wins |

Just as e-commerce didn't kill "retail" itself but killed "not-good-enough retail experiences" — AI isn't damaging "software" itself, but "mediocre differentiation." SaaS companies that survive on feature-stuffing and per-seat pricing are watching their moats get bypassed by AI-native competitors at one-tenth the cost. An AI-native CRM doesn't need hundreds of feature pages. A conversation interface suffices.

But AI Has a Variable E-Commerce Never Had

E-commerce never had a "free mall." AI has Llama, Qwen, DeepSeek.

These open-source models are rapidly closing the gap with closed-source frontier models. When DeepSeek V3 can deliver GPT-4-class performance at a fraction of the inference cost, the "AI tax" has a ceiling.

This makes the model layer's endgame unlikely to be "OpenAI wins everything." More probable is a two-tier structure:

- Closed-source frontier layer: serves scenarios needing maximum capability — complex reasoning, long-chain agent tasks, multimodal — priced per token

- Open-source commodity layer: serves 80% of routine use cases, with costs approaching zero (hardware depreciation only)

Open source keeps AI concentration from reaching e-commerce extremes. Amazon holds about 38% of U.S. e-commerce share, not 90%. AI model-layer share may be more fragmented, because open source continuously lowers the "good enough" threshold.

But application-layer concentration could be even higher. AI's network effects are stronger than e-commerce's: better models → more users → more data and revenue → more GPUs → better models. E-commerce was at least constrained by warehouse and delivery radius. AI has no physical buffer. Winner-take-all happens faster.

Who Eats, Who Drinks

Value distribution isn't binary "winners vs. losers." It's three tiers.

Tier 1: Infrastructure — Certain Winners.

GPUs (NVIDIA), foundries (TSMC), memory (Samsung/SK Hynix/Micron), cloud (AWS/Azure/GCP), data center power. The pick-and-shovel sellers profit regardless of who strikes gold. Samsung's Q2 profit is expected to jump 18× year-over-year; all three memory giants have market caps above $1 trillion. This isn't a bubble — it's the direct beneficiary effect of the AI infrastructure tax. This aligns with the RAMageddon logic we analyzed in the storage supercycle.

Tier 2: Models + Deep Applications — Head Wins, Middle Loses.

The winners aren't only OpenAI and Anthropic. The application companies truly capturing the dividend are AI-native — Cursor, Perplexity, Character.AI — unburdened by legacy cost structures, pouring everything into AI leverage.

The losers are traditional SaaS. Their moats — workflow configuration, system integration, user habits — are being bypassed by AI-native competitors. They must "AI-ify," but that means token costs replacing server costs. Worse, model capability jumps every 6 months: the feature you just shipped might come free in the next model release.

This is the AI version of "e-commerce hollows out the middle": it's not that AI is useless, but that AI makes "mediocre differentiation" worthless.

Tier 3: End Consumers — Short-Term Win, Long-Term TBD.

People who use AI gain superpowers. People who don't fall behind. Just as e-commerce consumers enjoyed lower prices while Main Street shops disappeared — the long-term structural costs (employment shifts, rising economic concentration) haven't been settled yet.

Three Takeaways for Enterprises

1. Build AI FinOps. Uber's lesson isn't "AI is too expensive." It's that engineers had zero visibility into usage. When AI tools shift from assistant to primary engine, usage spirals are inevitable. Make every team see its token bill. Give architectural decisions — model selection, context management, prompt caching — cost attribution.

2. Don't budget by "average AI spend per engineer." AI spending follows a bimodal distribution. 5% of power users may generate 80% of costs. Budgeting by average leads to two errors: overestimating the majority's needs, underestimating the minority's explosive consumption.

3. If your moat is "feature count," you're most at risk. AI is making feature-stuffing as a differentiation strategy obsolete. Your moat needs to be proprietary data, proprietary distribution, or community network effects. "Lots of features" isn't a moat in the AI era. It's a liability.

Coda

Anthropic's 5,000 people generate $47 billion in annualized revenue. That number is the best evidence of cost-structure rewriting in the AI era — AI isn't replacing engineers. It's making engineers who can harness AI extremely expensive, while making companies that can't harness AI extremely fragile.

The cheaper tokens get, the faster this divergence. Just as e-commerce drove the cost of opening an online store toward zero while brick-and-mortar rent never fell — not every store died, but the stores that survived had to offer something the online store couldn't.

The AI era is the same: not every company will lose. But the companies that survive will have to offer something AI can't — or become the one collecting the AI tax.

This is the third piece in the Token Economics series. Previous: When Tokens Stop Being Costs and Start Being Capital: The Economics of Tokenmaxxing 2.0 | The Great Token Retreat: When AI Bills Get More Expensive Than People.