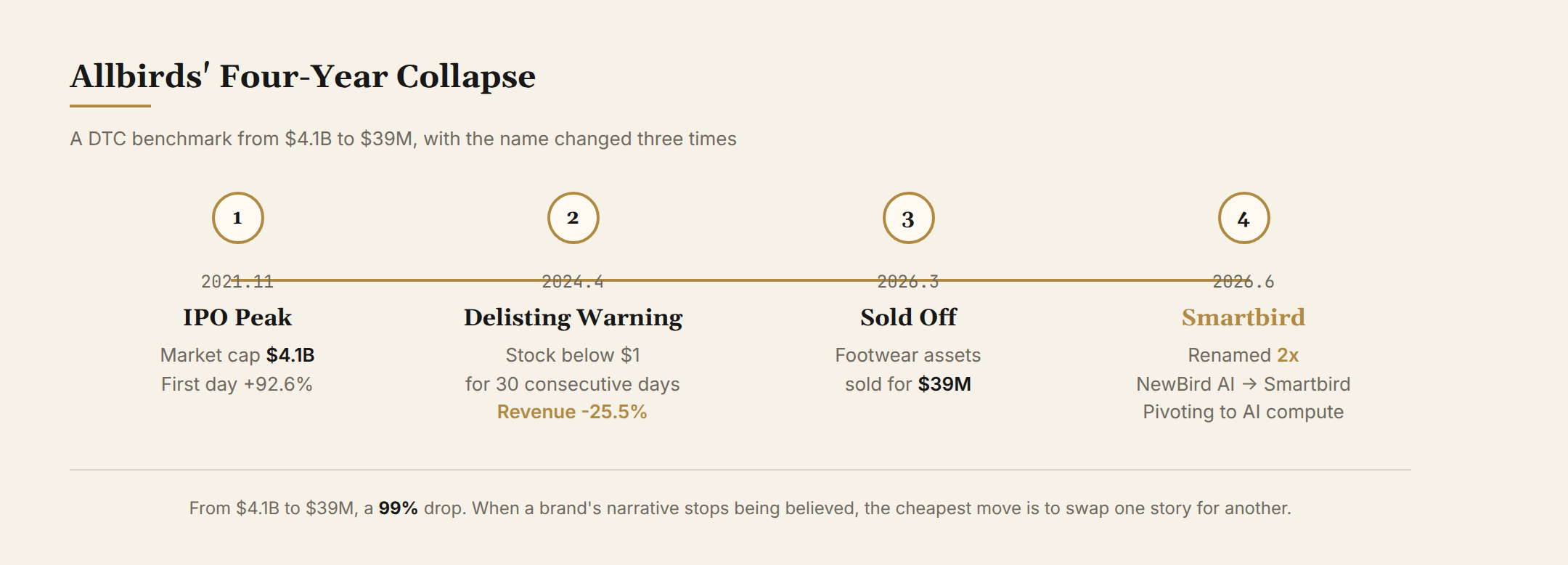

In June 2026, a wool-shoe company changed its name for the second time.

Allbirds announced it would rebrand to Smartbird and appointed Nadia Karsten, formerly of AWS quantum computing, as CEO. It was the second rename in two months: in April the company had already become NewBird AI, declaring a pivot from footwear to AI compute infrastructure. The stock (BIRD) jumped 41.88% that day.

A sportswear brand that hit a $4.1 billion market cap in 2021 sold its entire footwear business for $39 million three years later, then slapped an AI label on the shell.

This is not just one company running out of stories. Allbirds told the "eco-friendly merino wool sneaker" story for eight years. The last story was "we no longer make shoes." The problem: when a company's entire value sits on a narrative, the story ends and the company is left empty.

Allbirds' Real Problem: Marketing Without a Chassis

Allbirds was never just a marketing play. The starting point was a real product innovation.

In 2016, Tim Brown, a former New Zealand international footballer, and materials engineer Joey Zwillinger launched the Wool Runner. The upper was New Zealand merino wool with fibers 15.5–24 microns in diameter—about as fine as cashmere. The midsole used SweetFoam, a sugarcane-extract foam that Time magazine named one of the year's best inventions in 2018.

On foot, it genuinely felt different. Soft, warm, no break-in period, sockless-friendly, machine-washable. Silicon Valley queued up. Larry Page wore them. Tim Cook wore them. So did Barack Obama and Jack Ma. In 2018, the New York Times wrote: "Want to fit in in Silicon Valley? Wear these shoes."

In November 2021, Allbirds went public on NASDAQ. The stock popped 92.6% on day one, valuing the company at $4.135 billion.

But the IPO was the peak.

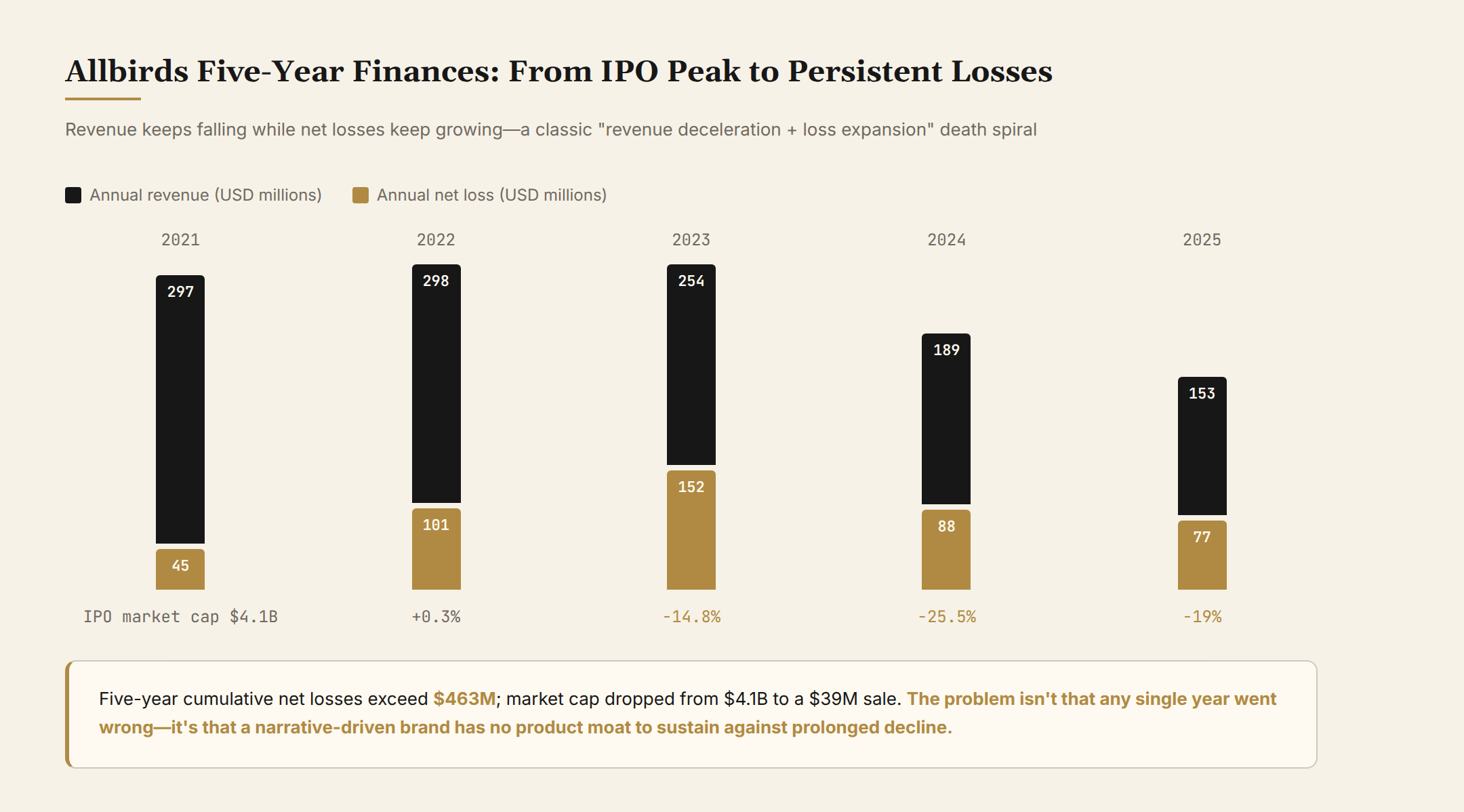

| Year | Revenue | Net loss | Key event |

|---|---|---|---|

| 2021 | ~$297M | ~$45M | IPO, $4.1B market cap |

| 2022 | ~$298M | ~$101M | Growth stalls |

| 2023 | ~$254M | YoY −14.8%, delisting warning received | −14.8% YoY; Nasdaq delisting warning |

| 2024 | ~$189M | ~$88M | YoY −25.5%; China rights sold to Belle |

| 2025 | ~$153M | ~$77M | YoY −19%; closed all U.S. full-price stores |

| 2026.3 | — | — | Sold footwear assets for $39M |

Five-year cumulative net losses exceeded $350M. Market cap fell from $4.1B to a $39M sale—a 99% drop.

Why?

The story was told too well, and the product not well enough. Allbirds wasn't selling shoes; it was selling the "eco + Silicon Valley + minimalist" narrative package. The product was genuinely good—but not deep enough:

- Sole too thin, sore on long walks

- Eight years, fifteen small tweaks to the Wool Runner, no technical depth

- Casual-commute category, inherently low-frequency consumption

- "Sustainability" is cognitive value, not experiential value—you feel the wool's softness, not the 30% lower carbon footprint

When a company's entire meaning sits on narrative (the eco story), the story ends and the company has nothing left but the shell. Allbirds' assets sold for $39M not because AI is better than shoes, but because the shoe story was done and the shoes themselves weren't worth that much.

Marketing-Driven Companies: When the Story Ends, So Do They

Allbirds is not an isolated case. The same script played out repeatedly during the 2015–2020 DTC wave.

Perfect Diary (Yatsen Holding): broke out on KOL (Key Opinion Leader) seeding on Xiaohongshu plus a "Chinese version of L'Oréal" positioning. 2020 IPO on NYSE, peak market cap ~RMB 160 billion (~$24B). Four years later, the stock had shed more than 90%. Perfect Diary lipsticks have no perceptible quality gap versus Florasis, Judydoll, or any other "luxury dupe." When the traffic stops, growth stops.

Zhongxue Gao: from 2017 the "Hermès of ice cream" narrative pushed a single bar to RMB 66. Its founder said in early interviews that "consumer demand for quality is infinite." In 2024, the company was exposed for unpaid wages and supplier bills, and the founder was put under consumption restrictions. From "infinite" to "infinitely in debt"—three years apart.

Casper: in 2014 the New York subway showed the "buy a mattress from the subway" ad. Five-year ride to IPO, peak market cap ~$1.1B. Then the D2C mattress market was eaten by Tuft & Needle, Purple, and other "product-power" mattresses. Market cap fell below $300M, taken private in 2022.

Genki Forest: relatively the winner, the erythritol-based formula cracked the "zero-sugar" category. But growth slowed sharply from 2022 onward as legacy beverage giants counterattacked.

The shared pathology: marketing first, product power second or third. When marketing carries the entire meaning of the brand, the story ends and the company collapses with it.

Product-Power-Driven Companies: The Story Doesn't Need to Be That Big

In the same wave, some survived—and grew into lasting companies.

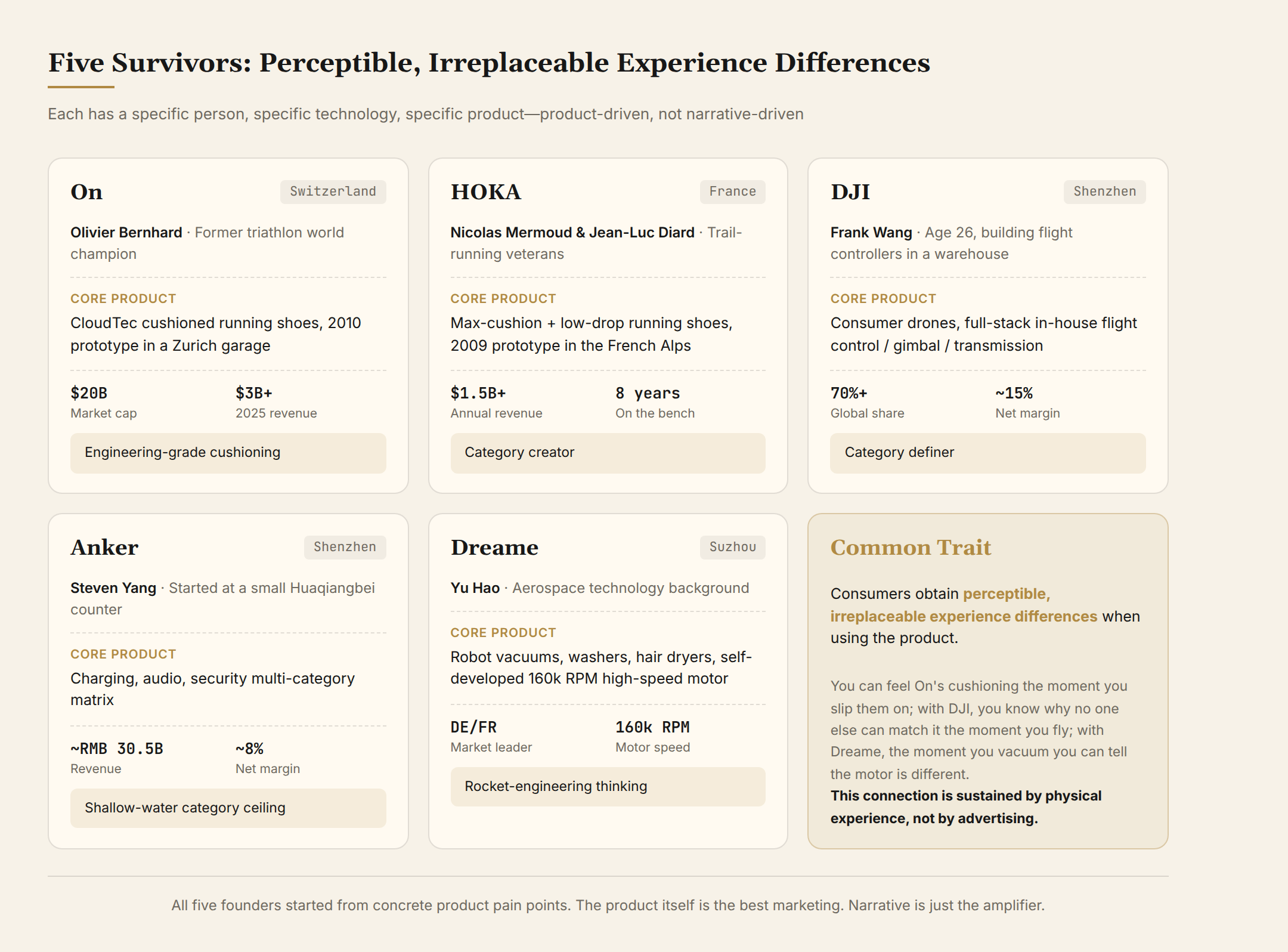

On: founder Olivier Bernhard is a former triathlon world champion. In 2010, in a Zurich garage, he and two friends built the CloudTec cushioning prototype—hollow "clouds" along the outsole collapse horizontally on landing to absorb impact, then lock and stiffen on takeoff to provide propulsion. The technology is a real engineering patent, not a story. On went public in 2021 and is now valued at roughly $20 billion—5× Allbirds' peak.

HOKA: Nicolas Mermoud and Jean-Luc Diard, two French trail-running veterans, built the first prototype in the French Alps: ultra-thick soles, yet ultra-light. Everyone said thick-sole running shoes had no future; they stuck with it for eight years. After being acquired by Deckers, revenue exploded past $1.5 billion a year. HOKA proved "professional athletic context + real biomechanical backing" is the only narrow gate that DTC can still squeeze through.

DJI: not a DTC brand, but the ultimate answer to "Chinese product power." Frank Wang was 26 when he was debugging the first generation of flight controllers in a warehouse; whenever the controller failed, he smashed it and started over, going through 30-plus units before stability. Full-stack in-house flight control, gimbal, transmission, camera. 5,800 patent applications. DJI doesn't sell through narrative—when you think consumer drones, you think DJI. Public estimates put 2024 revenue at ~RMB 60–80 billion, with a ~15% net margin (DJI is private; financials are public estimates).

Anker: Steven Yang started at a small counter in Huaqiangbei and grew the business to Amazon's #1 charging-bank category. 2024 revenue ~RMB 30.5 billion, ~8% net margin. Anker chose a shallow-water category—annual sales under $50B—where giants don't bother with you, but the ceiling is low.

Dreame: makes robot vacuums, scrubbers, and hair dryers, with a self-developed 160,000-rpm high-speed motor at the core. Founder Yu Hao comes from an aerospace background and brings rocket-engineering thinking to home appliances. It leads market share in Germany and France.

The common feature: consumers using these products get a perceptible, irreplaceable experience difference. Marketing is the amplifier—but the amplifier needs something underneath.

White Label Isn't Stealing the Low End—It's Filling the Product-Power Gap

Another form of marketing failure: the company doesn't collapse, but white-label products eat into its margin space in certain categories.

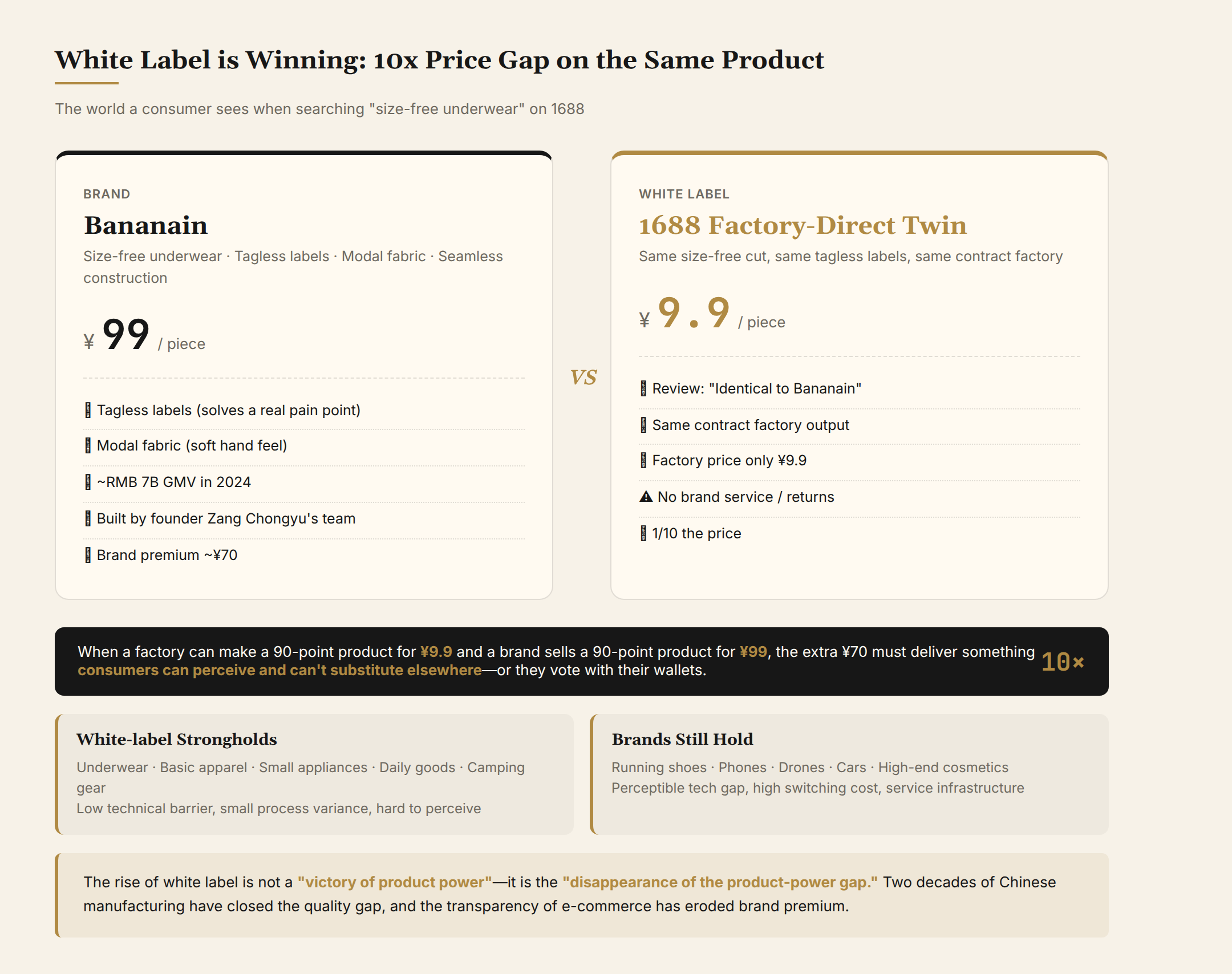

Bananain's founder said something his peers didn't want to hear in an interview last year: he fears not Uniqlo but "the surging white-label army against the backdrop of capacity overhang."

Bananain makes size-free underwear. "Tagless labels" sounds like a small innovation but it solves a real physical pain point. By 2024 GMV (Gross Merchandise Volume) reached nearly RMB 7 billion. The problem is that the underwear tech barrier is low to begin with—tagless labels, modal fabric, seamless construction, none of it is rocket science. You sell one piece for RMB 99; white-label sells for RMB 29. Most consumers can't tell the difference.

Open 1688 and casually search "size-free underwear." The RMB 9.9 factory-direct twin is everywhere. Reviewers post comparison shots with captions like "identical to Bananain."

Behind this are three structural shifts:

First, Chinese manufacturing maturation has closed the quality gap. The factories that OEM for international brands have fully accumulated process capability. Big brands and white labels often come off the same production line.

Second, the transparency of e-commerce platforms has been dissolving brands' "trust premium." A brand's old core value was "quality assurance." Today, reviews, teardown videos, side-by-side comparisons, and ingredient analyses are a tap away.

Third, consumers have redefined "good enough." A piece of underwear at ¥99 vs. ¥29—if the wearing experience differs by 10%, consumers in good times will pay 3× for the 10%. In down times, they won't.

The truth is: the rise of white label is not a victory of product power—it is the disappearance of the product-power gap. When a factory can make a 90-point product for ¥30, and a brand sells its 90-point product for ¥100, that extra ¥70 has to deliver something consumers can perceive and can't substitute elsewhere. Otherwise they vote with their wallets.

Marketing vs. Product Power: One Person's Day

Mapping all the companies we've discussed to the way they connect with consumers, there are essentially two kinds of relationships:

Marketing connection: tells a reason to buy—makes you feel "this is who I am when I buy this."

Product-power connection: the moment you put it on, you know "this thing is different."

The two can coexist, but only the latter can carry a company through decades.

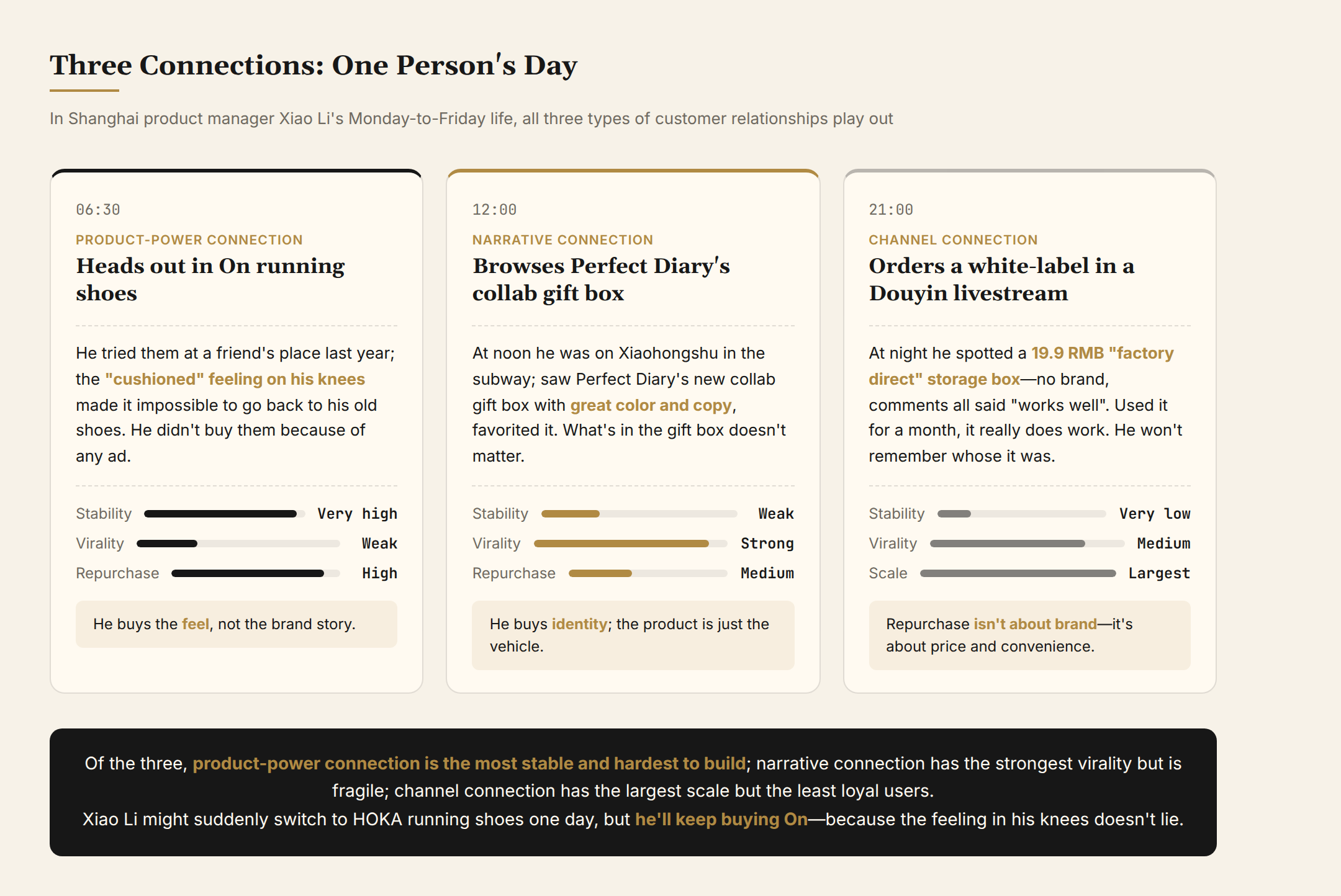

Xiao Li is an ordinary product manager in Shanghai. Both kinds of connections play out in his Monday-to-Friday life.

At 6:30 on Monday, Xiao Li puts on a pair of On running shoes and heads out. He didn't buy them because of any advertisement—last year he tried a pair at a friend's house, and the "cushioned" feeling under his knees made it impossible to go back to his old shoes. This is a product-power connection. Consumers buy the feel, not the brand story.

At noon, Xiao Li is scrolling Xiaohongshu in the subway and sees Perfect Diary's new collab gift box. The color and copy are on point, so he taps save. What's inside the box doesn't matter; what matters is "how I feel when I buy this." This is a marketing connection. Consumers' first reason to buy is identity; the product is just the vehicle.

At 9 p.m., Xiao Li is in a Douyin livestream and gets nudged into ordering a RMB 19.9 "factory-direct" storage box. No brand. Comments all say "works fine." It arrives, he uses it for a month, and it really does work. He doesn't know whose it is, and he'll never remember. This is a channel connection—marketing at its most extreme: not even a brand, just price and convenience.

Of the three, product-power connection is the most stable and the hardest to build. Marketing connection has the strongest virality but is fragile. Xiao Li might suddenly switch to HOKA running shoes one morning in 2026, or impulse-buy from some new brand's design on Xiaohongshu in 2027. But one thing doesn't change. What stays the same: he keeps buying On running shoes, because the feeling in his knees doesn't lie.

Product Power Is the Chassis. Marketing Is the Amplifier.

Tracing this whole sequence, a clear logic emerges:

Marketing is the amplifier. Without marketing, On wouldn't have become a Silicon Valley default, and lululemon wouldn't be synonymous with athleisure. Marketing is the key force that takes a brand from 0 to 1.

But marketing must sit on top of product power. On's CloudTec is an engineering patent, not a marketing line. lululemon's Luon fabric is a technical breakthrough, not a brand story. If the chassis isn't solid, no amount of marketing can hold up sustained decline—Allbirds told its story for eight years and finally sold the company to an AI-compute firm.

Product power is the chassis. It determines a company's floor: how long it can last, how deep a downturn it can absorb, whether it still has premium pricing space when white label encroaches. Even after the pandemic and commodity-price spikes, On kept growing, because the cushioning experience is a real difference.

White label isn't stealing the low end—it's filling categories where the product-power gap is too small. When a factory can make a 90-point product, the brand's "story premium" won't hold. What holds is the difference above 95 points, a difference consumers can clearly perceive.

Product power and marketing—either alone isn't enough. But product power is the chassis. When Allbirds sold itself for $39M, On was worth $20 billion and still selling shoes.

The Contrast: Same Day IPO, Five Years Later

Around November 17, 2021, Allbirds and On rang the IPO bell within days of each other. One told the story of "sustainability," the other of "cushioning." Both founders were worth hundreds of millions of dollars at the time.

Five years later, Tim Brown sold his company for $39 million, rebranded it Smartbird, and prepared to tell a new story about AI compute infrastructure. Olivier Bernhard's On is worth about $20 billion—5× Allbirds' peak.

This contrast is not an isolated case. It's a microcosm of the past decade's DTC wave:

- Allbirds told the "eco" story; the story ended, and the shoes stopped selling

- Perfect Diary told the "Chinese L'Oréal" story; the traffic stopped, the stock fell 90%

- Zhongxue Gao told the "Hermès of ice cream" story; unpaid wages, founder under consumption restrictions

- Casper told the "buy-a-mattress-from-the-subway" story; eaten alive by product-power mattresses

These companies didn't have product power? They did. But not strong enough that only "the story" was holding them up. When marketing carries the entire meaning of the brand, the story ends and the company is left empty.

The other side:

- On has kept growing post-IPO, $20B market cap

- HOKA sold thick-soled running shoes for eight years, $1.5B+ annual revenue

- DJI holds 70%+ global share, never relied on brand narrative

- lululemon has spent 30 years on fabric and community, no "disruptive narrative"

These companies didn't have marketing? They did. But marketing was the amplifier, and underneath sat product power. CloudTec, fabric, flight control, cushioning—the chassis is there, and that's what marketing amplifies.

Allbirds has isn't a brand—it's an advertising campaign running on a channel. When the ads stop, the campaign ends.

What On has isn't marketing—it's a shoe you can feel the moment you slip it on. When the marketing cycle fades, the shoe remains.

The market gave the same answer five years in a row: the story ends, the marketing stops; the product is there, the company lasts.

Disclosure: This article is based on public information, drawing on reporting from Tencent News, Sina Finance, Eastmoney, Baijia Hao, 36Kr, ZAKER, Xueqiu and others, plus public financials or public estimates from Allbirds / DJI / On. All company data as of June 18, 2026. The Smartbird renaming comes from public reports dated April and June 2026; DJI is private and its financials are public estimates for reference only. This is not investment advice.