On June 16, 2026, SpaceX acquired Anysphere — Cursor's parent company — for $60 billion in an all-stock deal. Just three days had passed since SpaceX's largest-ever IPO.

But the story didn't even wait 24 hours. On June 17, Cursor held its inaugural Cursor Compile conference in San Francisco, where CEO Michael Truell announced: 1.5 trillion+ parameters, 100K-GPU training, from scratch (not based on an open-source base model). Compute scaled 10-20x from before. Launch in weeks. He also revealed that Anthropic is the only company to have jumped to 10 trillion parameters (Mythos); Opus 4.5-4.8 and GPT-5-5.5 both sit below 2 trillion. This means 1.5T is already approaching Opus 4.8 / GPT-5.5 class in scale.

Taken together, these two events pose a question sharper than the acquisition itself: Do tool companies without their own models have an independent future? Cursor is the only living answer — but that answer requires four external conditions to be simultaneously met: self-training or open-source base capability, 100K-GPU-level compute capital, heavy RL investment, and a deal structure willing to surrender independence. Miss even one, and this path doesn't work.

Cursor's June two-step (May 18 Composer 2.5 + June 17 1.5T new model) proved the path is technically viable — but simultaneously proved its cost: it works only because Cursor sold itself to the only company that could give it 100K GPUs.

This is the real shape of the blurring boundary between "tool companies" and "model companies": tool companies aren't becoming model companies — they're being absorbed into them.

I. How the Landscape Formed

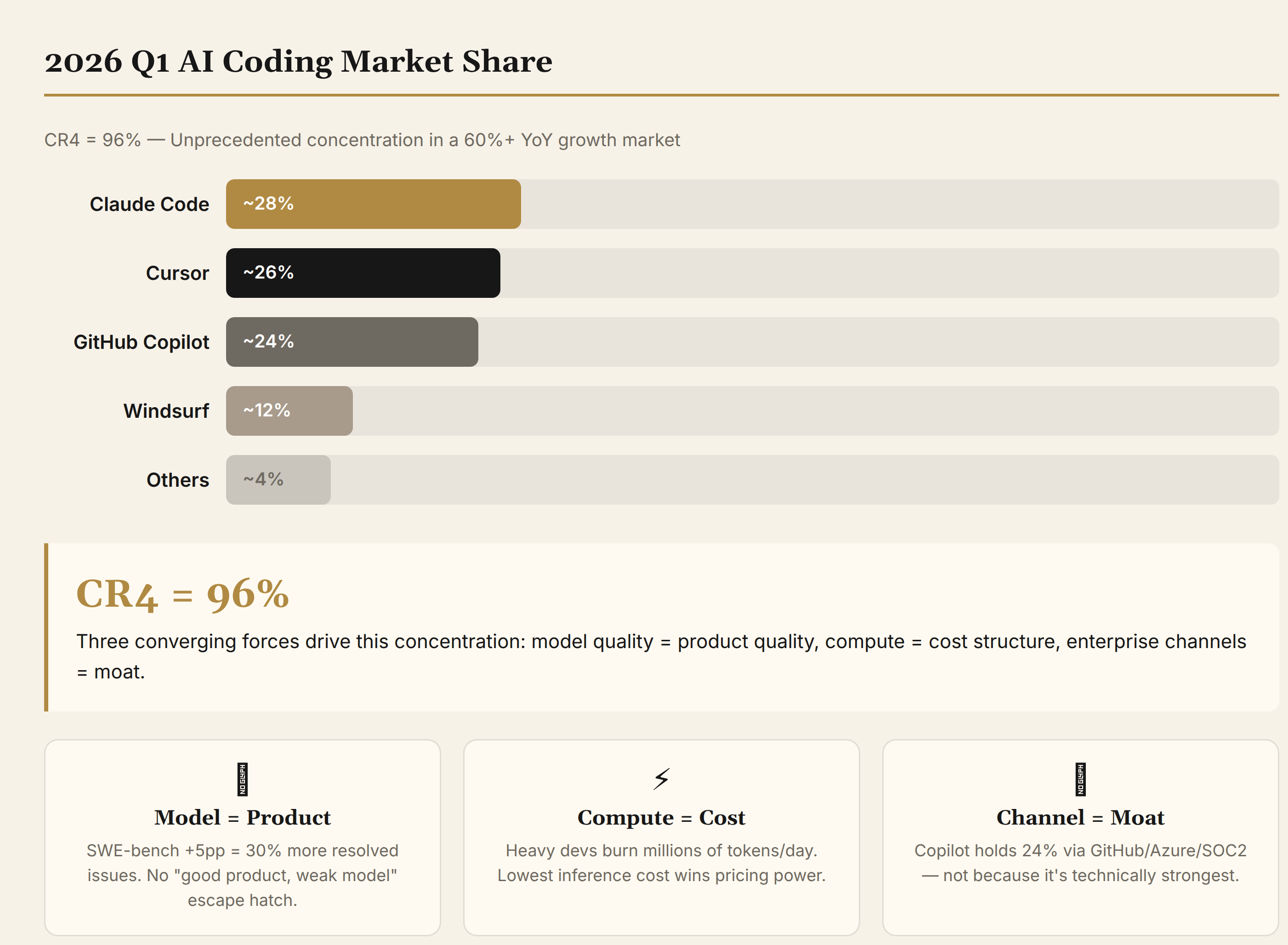

In Q1 2026, the CR4 of the global AI coding tool market reached 96% — Claude Code (~28%), Cursor (~26%), GitHub Copilot (~24%), Windsurf (~12%), with all other players splitting the remaining 4%. In a market growing 60%+ year-over-year, this concentration is abnormal.

Normal markets don't lock in structure during an explosive growth phase. AI coding went down this path because three forces converged simultaneously.

Model as product. Unlike the SaaS era, an AI coding tool's core capability is directly determined by its underlying model. Every 5 percentage point improvement in SWE-bench scores means roughly 30% more real GitHub Issues resolved independently. Anthropic's Opus series, from 4.0 to 4.7, turned each model release into a user growth inflection point for Claude Code. Model upgrade = product upgrade. Model lag = product lag. There is no "good product compensating for a weak model" escape hatch.

Compute as cost structure. AI coding is a high-frequency, long-duration tool. Token consumption far exceeds chat scenarios. A heavy developer might burn millions of tokens daily. Whoever pushes inference costs lowest gains pricing room. Claude Code runs on Anthropic's proprietary inference infrastructure, Copilot has Microsoft's global compute network, and SpaceX has Colossus 2's million-H100-equivalent compute. Cursor's May 18 Composer 2.5 and upcoming 1.5T model both run on this.

Enterprise channels as moat. GitHub Copilot holds 24% share at $10/month not because it's technically strongest — its SWE-bench score is the lowest among the top three — but because it's locked into the GitHub ecosystem, Azure DevOps, with SOC 2 Type II and ISO 27001 certifications. 1.8 million enterprise paying users won't switch because another tool scores 5 points higher on SWE-bench. This is Microsoft's scale advantage extending into the AI era.

These three forces — model gap, compute cost, enterprise channel — jointly drove AI coding toward extreme concentration. The middle ground is vanishing: either you own the full stack, or you survive in a narrow enough niche. After Google poached Windsurf's core team, Cognition picked it up for ~$250M, pivoting to SMB and Agent automation. Its 5% market share remains, but it's no longer a top contender. ByteDance's Trae grabbed 6 million registered users in China with a free strategy, but overseas influence is limited.

CR4 = 96% is not the endgame. This number will keep rising.

II. Did Cursor Fall Behind?

This question needs to be split in two.

Product Layer: No

If you only look at IDE experience, Cursor in 2026 is still the best.

The Supermaven engine's code completion is the industry benchmark — predictive multi-line completion that doesn't just autocomplete one line, but predicts entire function signatures and implementations based on project context. P50 latency under 300ms, faster than Copilot, and a completely different dimension compared to Claude Code (pure CLI, no completion). A developer accustomed to Cursor's Tab key feels "missing a hand" switching to any other tool.

Multi-model switching is another underestimated advantage. Developers can freely switch between Claude, GPT, and Gemini — even mixing them: Claude for complex reasoning, GPT for fast completion. Cursor users are never bottlenecked by one model's weakness. In Claude Code, you only use Claude. In Copilot, you mainly use OpenAI. Only Cursor gives developers real model choice.

Cursor 3's Glass interface, launched in April 2026, supports 8 Agents working in parallel on different file sets — frontend, backend, testing, documentation can all proceed simultaneously. In real tests, a project refactor requiring 120 minutes of serial work finished in just 18 minutes of parallel execution. This is genuine IDE-level innovation.

On the customer front: a 700-person team, serving 60% of the Fortune 500, with B2B annualized revenue of $2.6B (Reuters) to $4B (Forbes estimate). Whichever number you take, this is a company with real enterprise value.

Product layer: Cursor did not fall behind.

Structural Layer: From Being Left Behind to Catching Up — Cursor's June Two-Step

Before May, Cursor was pressed on three dimensions: model gap, Agent autonomy, and compute cost. Cursor's June two-step changed this story.

Step One: May 18 Composer 2.5. Three benchmark cross-evaluations: CursorBench v3.1 at 63.2% (exceeding Opus 4.7's default tier at 61.6%), SWE-Bench Multilingual at 79.8% (matching Opus 4.7's 80.5%), Terminal-Bench 2.0 at 69.3% (matching Opus 4.7's 69.4%). Priced at $0.5 per million input tokens and $2.5 per million output tokens — one-seventh of Opus 4.7's default tier. CEO Truell disclosed that 35% of Cursor's merged PRs are now created by autonomous Agents.

But Composer 2.5 is a "transitional product." It's based on Moonshot AI's Kimi K2.5 open-source checkpoint (1T-parameter MoE, 32B active per inference), with 85% of total compute invested in Cursor's own post-training and RL, introducing three innovations — text-feedback-based targeted RL (solving credit assignment in long rollouts), 25x the synthetic task volume of Composer 2, and Sharded Muon + dual-mesh HSDP (0.2 seconds per optimizer step on a 1T model); partial training ran on xAI's Colossus 2. This is a "Chinese base + proprietary RL + American compute" hybrid model.

Step Two: June 17, 1.5T new model announcement. Cursor Compile conference: 1.5 trillion+ parameters, 100K-GPU training, from scratch (not based on Kimi's open-source base — just two weeks ago, Composer 2.5 was being criticized for "wrapping Kimi"), compute scaled 10-20x from before, targeting general intelligence (not just code), launching in weeks. Truell also revealed: Anthropic is the only company to have jumped to 10 trillion parameters (Mythos); Opus 4.5-4.8 and GPT-5-5.5 both sit below 2 trillion. The 1.5T model is already approaching Opus 4.8 / GPT-5.5 class in scale.

Strategic significance of the two-step: Short-term shortcut (Composer 2.5 using Kimi base + RL to achieve Opus-level at 1/7 price), long-term capability building (1.5T from-scratch + 100K GPUs). This also explains why all the June moves (April agreement → June announcement → IPO → formal deal signing) are strongly correlated with the 1.5T model's compute requirements — Composer 2.5 is the "can hit Opus-level" capability proof for capital markets, while the 1.5T new model is the practical commitment to SpaceX: "I can consume your million-H100 compute."

III. Cursor's Fourth Path — And What It Cost

Before May, three paths lay before Cursor:

Path One: Build your own model. When Composer 2 launched, the capability gap with frontier models was obvious. Training a frontier model requires tens of thousands of GPUs and billions of dollars. At the Composer 2 stage, this path looked blocked.

Path Two: Partner with a giant. Deep integration with a company that has both models and compute. Options were limited: OpenAI has its own Codex and doesn't need Cursor; Google has Gemini Code Assist and Antigravity; Microsoft has Copilot. Only xAI needed Cursor — Grok's coding capability was far behind competitors. And behind xAI is SpaceX.

Path Three: Retreat to a niche. Focus on one segment — say, the best frontend development experience. This path lets you survive, but valuation drops from $50B to below $5B.

After June 17, Cursor carved out a fourth path: self-training a 1.5T+ parameter model + 100K-GPU compute + heavy RL + SpaceX-level compute partner.

But the cost of this fourth path was Cursor itself.

How much does 1.5T from-scratch cost. Industry experience: 1T parameters + 10T tokens training costs roughly $5-10B in compute alone, plus personnel, data, and debugging — single-run budgets in the $1-2B range. Cursor's B2B revenue is $2.6B; theoretically affordable — but 100K GPUs running for weeks (even at optimal utilization) puts single-run costs in the $5-10B range. Profit margins get eaten by compute bills.

The global supply list for 100K-GPU compute. The companies that can reliably supply 100K-GPU-level compute are few. xAI (Colossus has million-H100-equivalent; 100K GPUs is just 1/10 of that — available). Microsoft (Azure has scale, but Copilot is a direct competitor — won't give to Cursor). Google (has its own tool layer Antigravity; conflict of interest). Meta (open-source but not tool-related) and Amazon (already locked to Anthropic) are impossible. xAI is nearly the only option that can supply Cursor with 100K GPUs.

What team does from-scratch training need. Truell is 25 this year. Among Cursor's 700-person team, fewer than 50 can support 1.5T model training from scratch. A significant portion of those 50 were poached from Anthropic, Google, and OpenAI over the past year. Without $60B in capital backing and SpaceX's "bet-the-company" commitment, this team can't be retained.

The deal structure is key. Cursor got xAI's compute commitment not because there's a "compute market" to buy from, but because it signed a deal with xAI: "SpaceX either acquires us, or pays $10B breakup fee." This agreement was signed in April — Cursor exchanged a "won't sell to anyone else" commitment for xAI's compute commitment. The fourth path works not because Cursor can build it, but because Cursor can make itself acquirable.

Capability Acquisition ≠ Independent Exercise

Here's the critical distinction: Cursor acquired "training capability" (50-person core team + know-how + Composer 2.5 engineering experience), but exercising this capability depends on "compute supply" (100K GPUs), and the compute supply's only channel is xAI. In other words, Cursor can train models, but whether it trains, what it trains, and how many GPUs it uses — those decisions don't belong to Cursor.

This is the real shape of the blurred boundary between "tool companies" and "model companies": tool companies aren't becoming model companies — they're being absorbed into them. Tool companies acquired a "quasi-model-company" capability label, but the conditions for exercising this capability — compute — are monopolized by another company. Cursor's speech at the June 17 Cursor Compile conference was the clearest expression of this "absorbed quasi-model-company" articulating its own position.

Hugging Face CEO Clement Delangue's comment on Composer 2.5 — "Companies serious about AI will eventually train their own models, based on open source" — was already incomplete by June 17. What Cursor is doing now: training its own model, from scratch, at Opus/GPT-class scale — but the compute is someone else's, the capital is someone else's, and the ultimate ownership is someone else's.

IV. What $60B Bought

Four Layers of Assets

If SpaceX just wanted an IDE, it could build one or acquire an open-source project for $50M. The $60B didn't buy Cursor's editor — it bought four layers of assets:

Layer One: Enterprise customer channel. 60% of the Fortune 500 are Cursor customers. These enterprise relationships, security compliance audits, procurement contracts — building a sales team from scratch takes at least 3-5 years. SpaceX's IPO narrative is a $2.6 quadrillion AI market, where enterprise AI is the largest slice. Without an enterprise customer channel, this narrative is empty.

Layer Two: Developer community and talent. Cursor has a 700-person team including the best product engineers in AI coding — especially the ~50 who can run 1.5T model training. Cursor's brand in the developer community is positive — the pioneer of "AI-first IDE." This brand equity can't be replicated through hiring.

Layer Three: The compute monetization loop. xAI has Colossus 2's million-H100-equivalent compute, but lacks a channel to turn compute into coding revenue. Cursor is that channel. After the acquisition, Cursor users' compute can migrate from Anthropic/OpenAI/Google APIs to xAI's own Colossus — every code completion, every Agent execution becomes SpaceX's own revenue.

Layer Four: Model training capability + pipeline. This is the key asset that the June 17 Cursor Compile conference added for SpaceX. Cursor has proven it can, within three months, execute both a "Chinese base + proprietary RL + American compute" path (Composer 2.5) and a "from-scratch 1.5T + 100K GPUs" path (coming soon). SpaceX didn't just buy "a tool company" — it bought "an engineering team that can turn 100K-GPU compute into frontier models + frontier tools."

And the crucial step has already been taken: Cursor and xAI are already jointly training the next-generation model (1.5T), using "10x the total compute of Composer 2.5," running on Colossus 2-class infrastructure. The SEC filing for X67 Inc. — the subsidiary SpaceX established for the acquisition — shows the deal structure was designed long ago.

Is $60B Expensive?

By the numbers: Cursor's annualized revenue is $2.6-4B, so $60B valuation corresponds to 15-23x revenue. For a SaaS company, this multiple is high but not insane — high-growth SaaS frequently trades above 20x.

But this valuation can't be calculated purely on SaaS logic. SpaceX used freshly IPO'd stock ($135 issue price, now $211+), not cash. For SpaceX, $60B is roughly 2.4% of market cap. Exchanging 2.4% equity for an enterprise AI market entry ticket + a proven "100K GPU + from-scratch training" engineering team + a compute monetization loop — if the Cursor + Colossus combination works, this price is reasonable or even cheap.

The biggest risk isn't the price — it's model neutrality.

One core reason developers choose Cursor over Claude Code is multi-model switching — not being locked to one model. Post-acquisition, SpaceX has strong incentive to bias Cursor's model routing toward the 1.5T self-trained model / Grok series, reducing API dependency on competitors and costs. But if Cursor becomes a "self-trained model's dedicated IDE," developers will leave. Claude Code's developer satisfaction (Stack Overflow survey, 46%) is already 2.4x Cursor's. Once developers feel Cursor has lost neutrality, migration cost is far lower than the technical barrier of switching from Cursor to Claude Code.

SpaceX's smart play is to maintain Cursor's multi-model support — externally saying "we support all models" while making the 1.5T self-trained model cost-advantageous on its own compute. Compete on price, not forced lock-in. But this strategy's ceiling is determined by the 1.5T model's real capability — if it can genuinely deliver Opus-level performance, the cost curve is naturally advantageous.

Slightly expensive, but logically coherent. Success or failure doesn't hinge on price — it hinges on whether the 1.5T model can hit the level Truell promised when it launches in weeks.

V. Who's Next

If Cursor is the first tool company to trade independence for 100K-GPU compute via SpaceX, who comes next?

Four-Piece Analysis

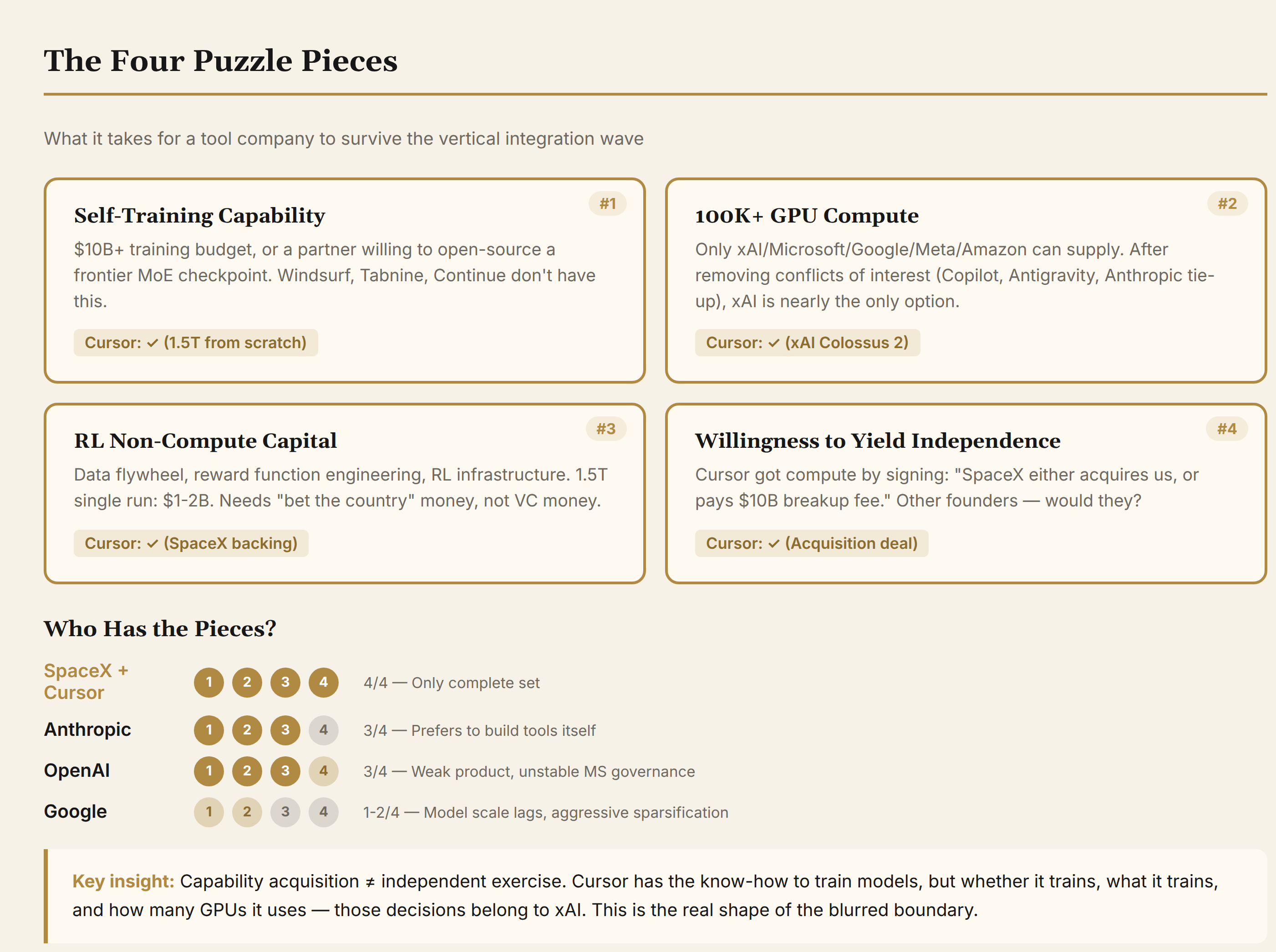

Composer 2.5 and the 1.5T new model together prove: the "build your own model" path is viable, but requires four puzzle pieces to align simultaneously. For other tool companies, all four are extremely difficult to assemble.

- Self-training or open-source base capability. Needs $1B+ training budget, or a partner willing to open-source a frontier MoE checkpoint like Moonshot AI. Windsurf, Tabnine, Continue don't have this.

- 100K-GPU compute capital. Globally, only xAI/Microsoft/Google/Meta/Amazon can reliably supply. After removing conflicts of interest (Microsoft has Copilot, Google has Antigravity, Meta isn't tool-related, Amazon is locked to Anthropic), xAI is nearly the only option. No independent tool company is on this list.

- Heavy RL non-compute capital. 1.5T single training run: $1-2B, with return cycles too long to explain to LPs. This requires SpaceX-style "bet-the-country" money, not ordinary VC capital. Specifically: data flywheel, reward function engineering, RL infrastructure investment — the non-compute spending.

- Willingness to yield independence. This is the most subtle piece — Cursor got xAI's compute commitment because it agreed to "either get acquired, or pay $10B breakup fee." Would other tool company founders accept this?

All four present: as of today, only the Cursor + SpaceX combination.

Remaining Players

Windsurf is already out. After Google poached its core team, Cognition picked it up for ~$250M, pivoting to SMB and Agent automation. Its 5% market share remains, but it's no longer a top contender.

GitHub Copilot has the most stable position, but the most obvious ceiling. Its enterprise ecosystem moat (GitHub/Azure/compliance certifications) makes it unacquirable and hard to displace. But $10/month anchors its positioning: the enterprise default, not the frontier choice. Microsoft's internal politics — Copilot vs Codex vs potential Xcode integration — make it hard to deliver Cursor-level product innovation.

Replit, Cognition, Devin — companies pursuing differentiation (Agent automation, education, full-stack automation) — aren't on the "pure tool company" death line for now. But model-level progress will keep eroding their space — when Claude Code's Agent can independently complete full projects, the boundary between "AI software engineer" and "AI coding tool" blurs.

Acquisitions Will Happen, But the Logic Has Changed

After the next reshuffle, "vertical integration" in AI coding won't be a simple story of "model company acquires tool company for an IDE." It will become "which super-compute company can assemble the next Cursor pattern."

Several companies have three of four pieces — Anthropic has the first three (self-training capability, 100K-GPU Mythos compute, heavy RL investment), but lacks the fourth (political willingness to let independent tool companies be absorbed — Anthropic prefers to build tools itself). OpenAI has the first three but relatively weak product capability, with a contested fourth (Microsoft-OpenAI governance itself is unstable). Google's first two pieces are discounted (Truell noted in his speech that "model scale wasn't pushed to comparable levels, sparsification route was overly aggressive"), and the third and fourth pieces don't work.

All four pieces present: currently only the SpaceX + Cursor pair. This is also why $60B looks expensive but logically only SpaceX could afford — no second company can replicate the "compute + 100K GPUs + independent tool company willing to sell" combination.

The next most likely target isn't a "tool company" — it's a middleware company that can fill a missing piece. Like a Chinese model company willing to open-source the strongest MoE base (DeepSeek, Zhipu GLM) — sold to SpaceX to fill the "open-source base" piece; or a small team with edge deployment/localization capability, needed by Anthropic to fill its "localization soft spot." The core of the Cursor pattern isn't "buy a tool" — it's "assemble four puzzle pieces."

The Four-Piece Logic Extends Beyond Coding

Cursor is the first tool company to be swallowed by this logic, but it won't be the last. The same forces — model as product, compute as cost, independence getting more expensive — are pressuring every tool domain where core capability is determined by the underlying model. Extending the four-piece framework reveals different levels of vulnerability.

AI Search (Perplexity) — highest similarity to Cursor. Perplexity has $500M annualized revenue, 100M MAU, and a $20B valuation, with the CEO announcing plans for a 2028 IPO. But it faces the exact same structural problems as Cursor: search quality is directly determined by the underlying model, it has no frontier model of its own, and it depends on multi-model APIs. It's already partnering with CoreWeave for GB200 clusters for inference — but this is far from 100K-GPU scale. Perplexity building a browser (Comet) and Agent (Perplexity Computer) follows the exact same logic as Cursor building an IDE: tool-layer companies trying to maintain independence by owning the entry point. But if model companies decide to build their own search layer — Anthropic's search competitor, OpenAI's ChatGPT search — Perplexity's multi-model advantage becomes a multi-model liability: every provider can cut API access or raise prices.

AI Video Generation (Runway / Pika) — more compute-intensive than coding. Every video generation inference runs a diffusion model; training costs are an order of magnitude higher than LLMs. Runway's Gen-4.5 "world model" narrative is ambitious, but training costs are so large that only super-compute companies can afford them. Kling has Kuaishou's compute infrastructure as a moat; Runway and Pika don't. The "Cursor moment" for video tools may arrive faster than for coding — once a model company's Veo or Sora is good enough, independent video tool survival space shrinks dramatically.

AI Legal (Harvey) — deeper moat, but narrowing ceiling. Harvey is valued at $11B, serving 500+ top law firms with 25,000+ custom Agents running on its platform. Its moat is deeper than Cursor's: legal compliance certifications, firm procurement contracts, proprietary workflows — these aren't things model upgrades can directly erase. But Anthropic is already building legal-specific Claude, and the DXC alliance is embedding Claude in banking and aerospace core systems. Once models are strong enough that "general AI + legal plugin" ≈ "specialized legal AI," Harvey's independent value drops from "irreplaceable" to "has a nice data layer." It won't be forced to sell like Cursor, but its independent ceiling is lowering.

AI Agent Middleware (LangChain / CrewAI / AutoGen) — most easily erased by model upgrades. These companies orchestrate and schedule between models and end products; their value proposition is "help you manage multi-model collaboration." But when models natively support multi-step reasoning, tool use, and million-token context, the middleware layer gets absorbed directly. Claude Code is Anthropic's productized Agent middleware — it doesn't need LangChain.

Conversely, domains less likely to be targeted share common characteristics: the tool layer itself has deep intrinsic value (Figma's collaboration network effects), regulatory barriers are too high (healthcare/financial vertical SaaS), or models are merely an enhancement layer, not the core (Canva's design template library). These tool companies face a different pressure — not "get acquired," but "how to keep charging when AI capability becomes free infrastructure."

To summarize: AI coding is the first domino of vertical integration, but not the last. AI search and AI video are the two most vulnerable domains under the same logic — both are "model as product, compute as cost" structures. AI legal has a deeper moat but faces a narrowing ceiling. The four-piece framework doesn't just explain Cursor's fate — it's a universal analytical tool: any AI tool domain where core capability is model-determined, compute is the primary cost, and independence keeps getting more expensive will face the same vertical integration pressure.

Cursor's $60B gave a clear answer to "build a tool or buy one." But the more precise version is: "Are you buying a tool, or buying an engineering team that can turn 100K-GPU compute into a frontier model?" Composer 2.5 is the transitional minimum viable unit, the 1.5T new model is the endgame commitment, and $60B is the price of this path after capitalization.

After the next reshuffle, the AI coding space will likely only have two types of players remaining: "super-compute company + tool company" combinations that can assemble the next Cursor pattern, and independent tool companies surviving in vertical niches. The middle ground — "ordinary tool companies" that have neither compute nor willingness to be acquired — will be rapidly cleaned out. Whether Replit's differentiation can constitute a third category depends on whether it can find its own compute supply solution.

Who will SpaceX buy next? The answer is most likely: the next tool company that can assemble all four puzzle pieces. But tool companies that can simultaneously nail "open-source/self-training + 100K GPUs + RL capital + sell-out deal" within weeks won't be many.