The $14B Bet: A Strategic Landscape Analysis of HPE Discover 2026

In 2014, HPE was still part of HP. That year, HP's annual revenue was $111.4 billion, spanning everything from printers to servers, enterprise software to cloud services. Then CEO Meg Whitman made a decision: split the company into two — HP Inc (printing + PCs) and Hewlett Packard Enterprise (enterprise).

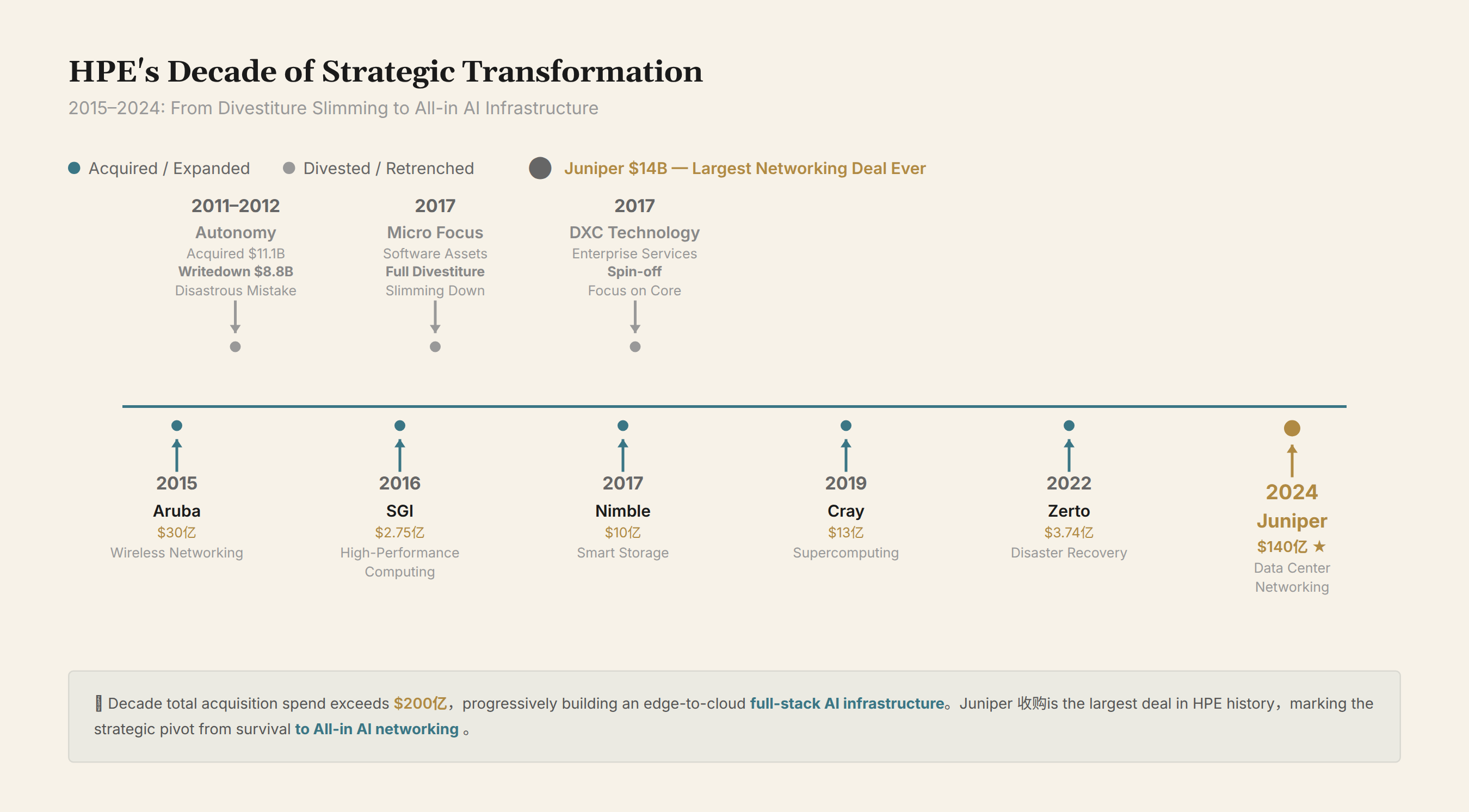

Over the decade since HPE became independent, its strategy can be distilled into a single sentence: Sell off unprofitable software businesses, and use the savings to buy networking and supercomputing companies.

What did it sell? Autonomy ($11.1B acquisition → $8.8B write-down → spun off to Micro Focus), the HPE Software division (divested in full), TES (testing services). What did it spin off? Enterprise Services (merged into DXC Technology), Consulting Services (merged into Perspecta).

What did it buy? Aruba ($3B, 2015, wireless networking), SGI ($275M, 2016, high-performance computing), Cray ($1.3B, 2019, supercomputing), Nimble Storage ($1B, 2017, all-flash storage), Zerto ($374M, 2022, disaster recovery), Juniper Networks ($14B, 2024, data center networking).

Over ten years, HPE transformed from a sprawling conglomerate into a sharply focused infrastructure company: compute (ProLiant + Cray), networking (Juniper + Aruba), storage (Alletra + Nimble), and operations software (GreenLake + Mist) — four business lines, one consumption brand (GreenLake).

The June 2026 Discover conference is the checkpoint for this journey. For the first time, HPE put all new products from its four business lines on the same stage — and CEO Antonio Neri needed to answer: what exactly has been formed by piecing together these companies, acquired at a cost of tens of billions of dollars?

Neri's Three Judgments

The keynote centered on three judgments, building one upon the other.

Judgment 1: The Network Is the Control Plane of AI Infrastructure

"There is one element that continues to be at the core of everything in infrastructure, and that element is the network."

The context for Neri's statement: over the past three years, everyone discussing AI infrastructure has focused exclusively on GPUs. NVIDIA's market cap soared from $300 billion to $3 trillion on the back of GPUs. But Neri pointed to an industry pain point — in 10,000-GPU training clusters, 30–50% of the time is not spent on computation but on waiting for data. No matter how high the GPU FLOPS, if the network can't keep up, the compute units idle.

HPE translated this judgment into products: the QFX switch series covering everything from training to inference to the edge, plus GreenLake Intelligence handing network operations over to AI.

But this judgment comes with a premise HPE is less comfortable stating outright: HPE has no control at the networking silicon layer. The core switching ASICs in the QFX series come from Broadcom. The companies that truly define the future of data center networking at the silicon level are NVIDIA (Spectrum-X) and Broadcom (Tomahawk 6). HPE is a systems integrator, not a chip definer.

Judgment 2: The Essence of an AI Factory Is Converting Electricity into Tokens

"At its core, an AI factory does one thing: convert electrical power into tokens."

This is not literary embellishment. A single GB300 NVL72 rack draws over 120 kilowatts — a data center filled with 50 such racks has power requirements comparable to a small power station. Neri cited two figures: the U.S. will face a 19-gigawatt power shortfall by 2028; data centers will account for nearly half of total U.S. electricity consumption by 2031.

HPE's moves in this direction: liquid cooling technology (inherited from Cray) + a Siemens Energy partnership (using AI tools to accelerate power grid engineering design). But HPE is essentially a supplier of token-conversion machines, not a power supplier. It makes liquid cooling hardware (it has products), does AI-assisted grid design (it has partnerships), but doesn't touch power generation or transmission.

Judgment 3: IT Departments Will Manage Thousands of AI Agents

"IT departments will be responsible for managing thousands of agents that are part of the enterprise workforce."

This is the boldest of the three judgments. It redefines AI agents from "applications" to "workloads" — requiring compute resources, storage access, network communication, security isolation, and lifecycle management.

HPE's product response: ProLiant DL 394 Gen 12 (agent-dedicated servers), an agent governance layer in private cloud AI (registration/identity/permissions/rollback), and Alletra MPX 10000's native MCP storage (agents retrieve data directly).

But the architectural standards for agents are not in HPE's hands. MCP belongs to Anthropic, the Actions API belongs to OpenAI, and LangChain belongs to the open-source community. HPE does the hosting layer — running agent architectures defined by others on its own hardware.

The Three-Brand Reorganization: Juniper / Aruba / Mist

After the $14 billion acquisition of Juniper, HPE's networking division has been fully reorganized into three independent brand lines:

| Brand | Origin | Coverage |

|---|---|---|

| Juniper | Acquired 2024 | Data center AI networking (QFX series), carrier-grade routing (PTX/MX), data center interconnect |

| Aruba | Acquired 2015 | Campus switches, wireless APs, SD-WAN, SASE security |

| Mist | Acquired by Juniper 2019 | AI operations platform (Marvis virtual assistant, Mist AI wireless/wired management) |

The three lines operate independently with a unified product roadmap. HPE's logic: customers in different scenarios have different needs (data center vs. campus vs. AI operations), and keeping independent brands helps with customer recognition and sales coverage.

But this structure has a potential friction point: blurry product boundaries. QFX switches sit under the Juniper brand but also get onboarded into the Mist platform. Aruba CX switches are now also onboarded into Mist. Customers will be confused at purchase time: which brand's product am I actually buying? How do the three brands' sales teams split the revenue?

Neri said in the media Q&A that this is "one of the smoothest large-scale integrations in HPE history." Analysts also gave positive assessments — Steven Dickens of HyperFrame Research said "HPE is now clearly a networking company," and Ron Westfall said the integration is progressing smoothly.

But "looking good" is not a reliable metric in tech M&A. Autonomy was also described as strategically complementary when announced. The real test will be the 2027 revenue numbers: Juniper's customer retention rate, cross-sell rates for new products, and whether brand conflict impacts orders.

HPE's Software Strategy: No General-Purpose Software, Only Infrastructure OS

The Pivot from Autonomy to GreenLake

HPE's software capabilities have long been questioned by the industry. The reason is easy to understand — Autonomy is one of the largest software debacles in tech industry history. HP acquired Autonomy in 2011 for $11.1B, wrote down $8.8B a year later, and accused the former of financial fraud. After this disaster, HPE divested its entire enterprise software business to Micro Focus.

Post-2015, HPE took a completely different software path: no general-purpose software (enterprise apps, big data, AI frameworks), only infrastructure management software.

The logic of this path: HPE's core customers are CIOs and IT operations teams. What they need is not another application platform, but tools to manage increasingly numerous and complex infrastructure.

The 2026 Software Landscape

After a decade of acquisitions and integration, HPE's software landscape is entirely concentrated in infrastructure operations:

| Layer | Product | Origin | What It Does |

|---|---|---|---|

| AI Ops Engine | GreenLake Intelligence | HPE in-house | Unified global telemetry analysis, AI-driven issue identification + recommendations + execution |

| Network AI Assistant | Marvis AI | Juniper→Mist | Natural language interactive network operations |

| Wireless/Wired Ops | Mist AI | Juniper | AI-driven management of APs and switches |

| Campus Management | Aruba Central | HPE | Unified campus switch/AP management |

| Data Center Ops | Apstra | Juniper | Data center network configuration automation |

| SASE Security | Aruba + Juniper | HPE | Cloud-delivered secure access services |

| Hybrid Cloud Management | CloudOps + Morpheus | HPE | Virtualization + data protection + cloud management |

| Agent Governance | NVIDIA Open Shell + NeMo + Zerto | Partner + Acquisition | Agent sandbox + workflow blueprints + state rollback |

Compared to Dell, HPE's software positioning is narrower but more focused — Dell is trapped by the VMware/Broadcom ecosystem; HPE has no such baggage. Compared to Cisco, HPE's software is more concentrated on network operations (Cisco bought Splunk for full-stack observability, broader in scope but more complex to integrate).

The Core Challenge: Integration Hell

The biggest problem in HPE's software landscape isn't a lack of products — it's too many products from too many disparate sources.

GreenLake Intelligence claims it will unify five platforms: Marvis, Mist, Aruba Central, Apstra, and CloudOps. These five platforms come from three different acquisitions (Juniper, Mist, Aruba), plus two HPE in-house systems. Each platform has its own:

- Data model (how network device states are described)

- API design (how external systems invoke it)

- Alerting logic (what conditions trigger what notifications)

- Automation workflow (how to auto-remediate after discovering an issue)

- User interface (what operations personnel see)

Unifying these five platforms into a single AI engine — this is an extraordinarily difficult engineering task. HPE has no historical track record of successfully integrating software assets at this scale. Autonomy was a failure (written down), Compaq was eventually split off. Can the Juniper + Aruba + Mist integration break the historical pattern?

From the public information at Discover 2026, the current integration progress is: UI layer (unified console) preliminarily complete, data layer (telemetry format standardization) in progress, AI layer (one model understanding all data) not yet started. An optimistic estimate puts the "self-driving" goal HPE describes at 2–3 years away.

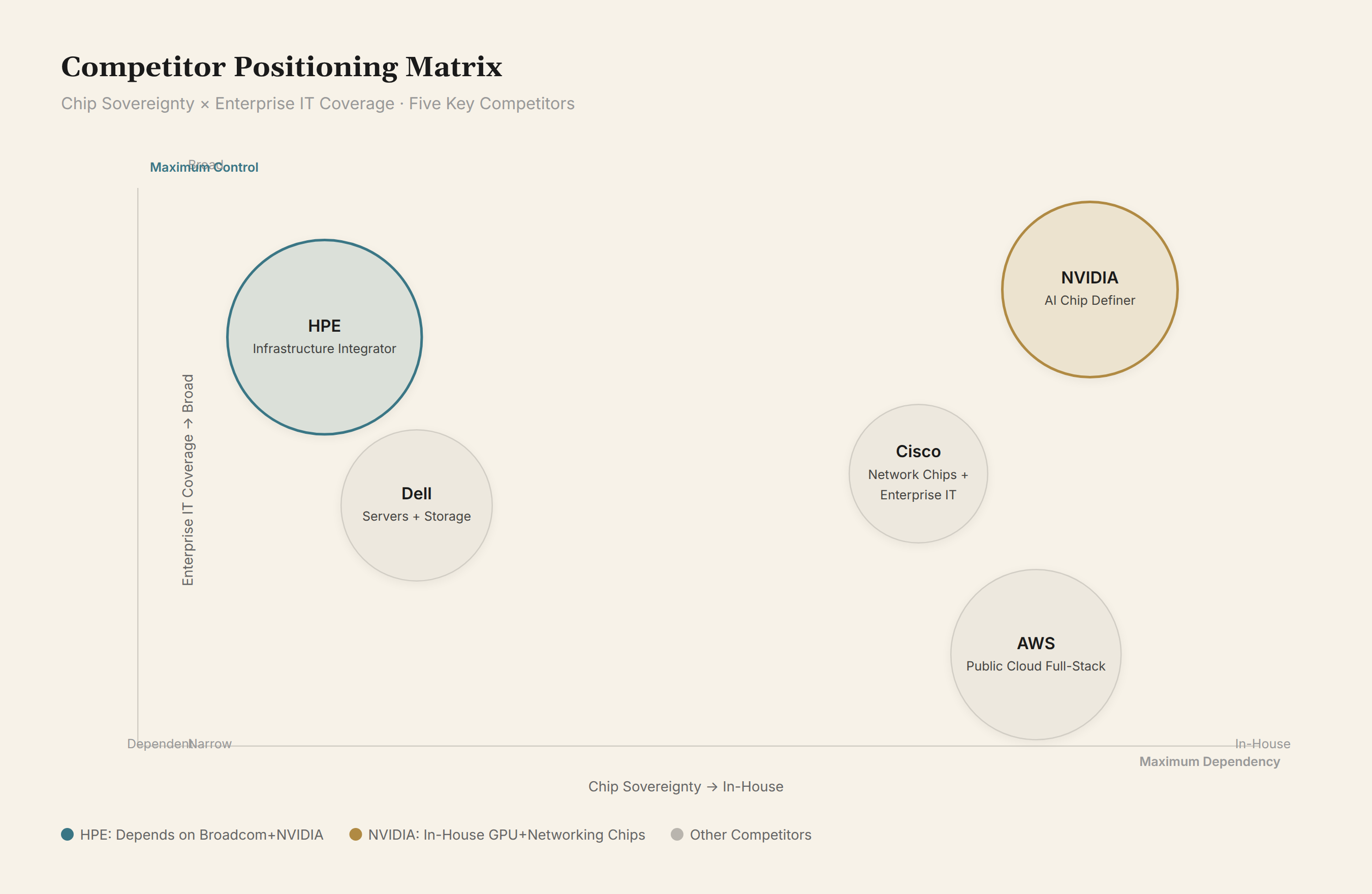

Competitive Positioning: Not Trying to Be the Next NVIDIA

The signal HPE sent at Discover 2026 was unambiguous: it's not trying to be the next NVIDIA (doesn't touch chips or models), not trying to be another AWS (doesn't do public cloud), but aiming to be the "infrastructure operating system for the AI era."

Can this positioning hold up in the market? Let's compare against several key competitors:

vs. NVIDIA

NVIDIA is the core definer of AI infrastructure — GPU (compute) + Spectrum-X (networking) + CUDA (software ecosystem) + DGX Cloud (full-stack delivery). HPE's relationship with NVIDIA is "partner + competitor": HPE uses NVIDIA's GPUs and Open Shell/NeMo to build its own AI factories, but NVIDIA's DGX Cloud and full-stack solutions compete directly with HPE.

Key difference: NVIDIA has silicon design ownership; HPE does not. NVIDIA's margins and strategic room will always exceed HPE's. But NVIDIA is not an enterprise IT supplier — it doesn't sell campus networking, doesn't do storage, doesn't do hybrid cloud management. HPE's enterprise IT coverage far exceeds NVIDIA's.

vs. Dell

Dell is HPE's most direct peer. Both do servers, storage, and networking. But Dell's networking business is weak (no proprietary switch product line, relies on partners like NVIDIA/F5), while its storage is strong (PowerScale, PowerMax). Dell is entangled in the VMware/Broadcom equity and pricing mess; HPE has no such baggage.

Dell leads in AI server market share (IDC data shows Dell as #1 in AI server shipments), but HPE, through the Juniper acquisition, has built a networking advantage that Dell cannot match.

vs. Cisco

Cisco is the incumbent leader in networking, but its AI story differs from HPE's. Cisco has proprietary switching silicon (Silicon One); HPE does not. Cisco bought Splunk for observability, competing with Mist AI at the operations layer. But Cisco's presence in AI servers is weak — it doesn't make GPU servers.

Cisco and HPE compete head-to-head at the networking layer (Silicon One vs. QFX), don't compete at the server layer (Cisco UCS only does general-purpose servers, not AI GPU servers), and don't compete at the storage layer (Cisco doesn't do storage).

vs. Cloud Providers

AWS, Azure, and GCP represent an alternative path for AI infrastructure — customers use GPUs and managed services in the cloud, without needing to build their own AI factories. HPE's positioning is to help enterprises build "private AI factories," making it a substitute for cloud providers.

But Neri also acknowledged a trend in his keynote: "Hybrid strategies are replacing either/or." More and more enterprises are using both private and public cloud simultaneously — core data and training in private AI factories, elastic inference workloads in the cloud. HPE's GreenLake consumption model sits squarely on this trend.

Ten Challenges

Examining HPE Discover 2026 against the industry backdrop reveals ten structural risks.

1. No differentiation at the silicon layer. QFX switching ASICs come from Broadcom. GPUs come from NVIDIA. HPE has no in-house capability in the two most critical chip categories. Systems integration is value, but integration margins will never match silicon-definition margins.

2. Software integration hell. Five operations platforms unified into one AI engine — extreme engineering difficulty, and HPE has never succeeded at this historically.

3. Three-brand structure may conflict. Juniper, Aruba, and Mist operate independently with blurry product boundaries and unclear sales incentive allocation.

4. Narrow QFX5140 delivery window. Announced mid-2026, actual shipments may not begin until late 2026. Broadcom Tomahawk 6 is already shipping in Cisco/Arista products during the same period.

5. NVIDIA is both partner and competitor. HPE uses NVIDIA GPUs + Open Shell + NeMo Cloud, but NVIDIA's DGX Cloud competes directly with HPE AI Factories. NVIDIA holds the dominant position in the partnership.

6. The energy narrative is hard to land. Neri says "convert electricity into tokens," but HPE only sells liquid cooling hardware and AI-assisted grid design tools — it doesn't do power generation or transmission.

7. The Cray legacy is being rendered invisible. Discover 2026 had no new supercomputing system announcements. The Cray brand is being folded into the AI factory narrative. Traditional HPC customers (DOE, universities) may turn to Lenovo or Atos.

8. DL 394 Gen 12 lacks specifications. Positioned as "agent-dedicated" but no public GPU slots, memory bandwidth, or power consumption figures — customers can't benchmark against Dell XE9680.

9. Customer lock-in risk. GreenLake's consumption-based model means deep HPE ecosystem lock-in. AI-era CIOs lean toward multi-vendor strategies and are reluctant to bet everything on a single vendor.

10. Agent standards are not in HPE's hands. MCP belongs to Anthropic, the Actions API to OpenAI, LangChain to open source. HPE does the agent hosting layer; it doesn't define agent architecture. The one exception is Alletra MPX 10000's native MCP storage — if MCP becomes a standard, this is a first-mover advantage.

Conclusion: The Right Direction, a Heavy Burden of Execution

HPE's path over the past decade is clear: sell software, buy networking and supercomputing, and unify the consumption brand under GreenLake. Discover 2026 is the first panoramic report card on this journey.

The directional judgments are correct:

- The bottleneck in AI clusters is indeed shifting from per-card compute to networking and storage I/O

- Agents are indeed transitioning from applications to workloads

- Enterprises indeed need private AI deployment (data sovereignty, compliance, cost control)

But judging correctly and executing correctly are two different things. The list of challenges facing HPE is long: silicon-layer dependency, five operations platforms to integrate, no clear product roadmap for Cray's technical legacy, and agent standards controlled by software companies.

Neri said something in his keynote that I think is the most honest line: "Every byte, every token, every decision traverses the network." — This describes a fact, not an ambition. HPE knows its place: it's not NVIDIA making chips, not OpenAI making models, not AWS making cloud. It is the layer that strings these companies' products together, adds operations software, and delivers them to enterprise customers.

This positioning has a market — global enterprise IT spending is $4 trillion, and not every company wants to assemble everything themselves. But the ceiling of this positioning is also clear: an infrastructure integrator's margins will always be lower than those of core technology definers. HPE can strive to be the best at the integration layer, but it cannot change the fact that it is not a chip company, not a model company.

Discover 2026 presented an HPE pointed in the right direction. The 2027 revenue numbers will tell us whether that direction can turn into a business.

Disclosure: This article is based on public coverage of HPE Discover 2026, drawing comprehensively on reports from Zhiding Technology, Tencent News, Qiehao, and other media outlets. HPE historical M&A data comes from public financial reports and news coverage. Competitive analysis is based on publicly available vendor materials. This does not constitute investment advice.