Morgan Stanley's Howard Kao team published a comprehensive BOM (Bill of Materials) teardown of NVIDIA's next-generation Rubin VR200 NVL72 rack on May 21, 2026. This isn't just a cost estimate — it reveals a structural inflection point in AI hardware economics.

$7.8 Million Per Rack: Where Does the Money Go?

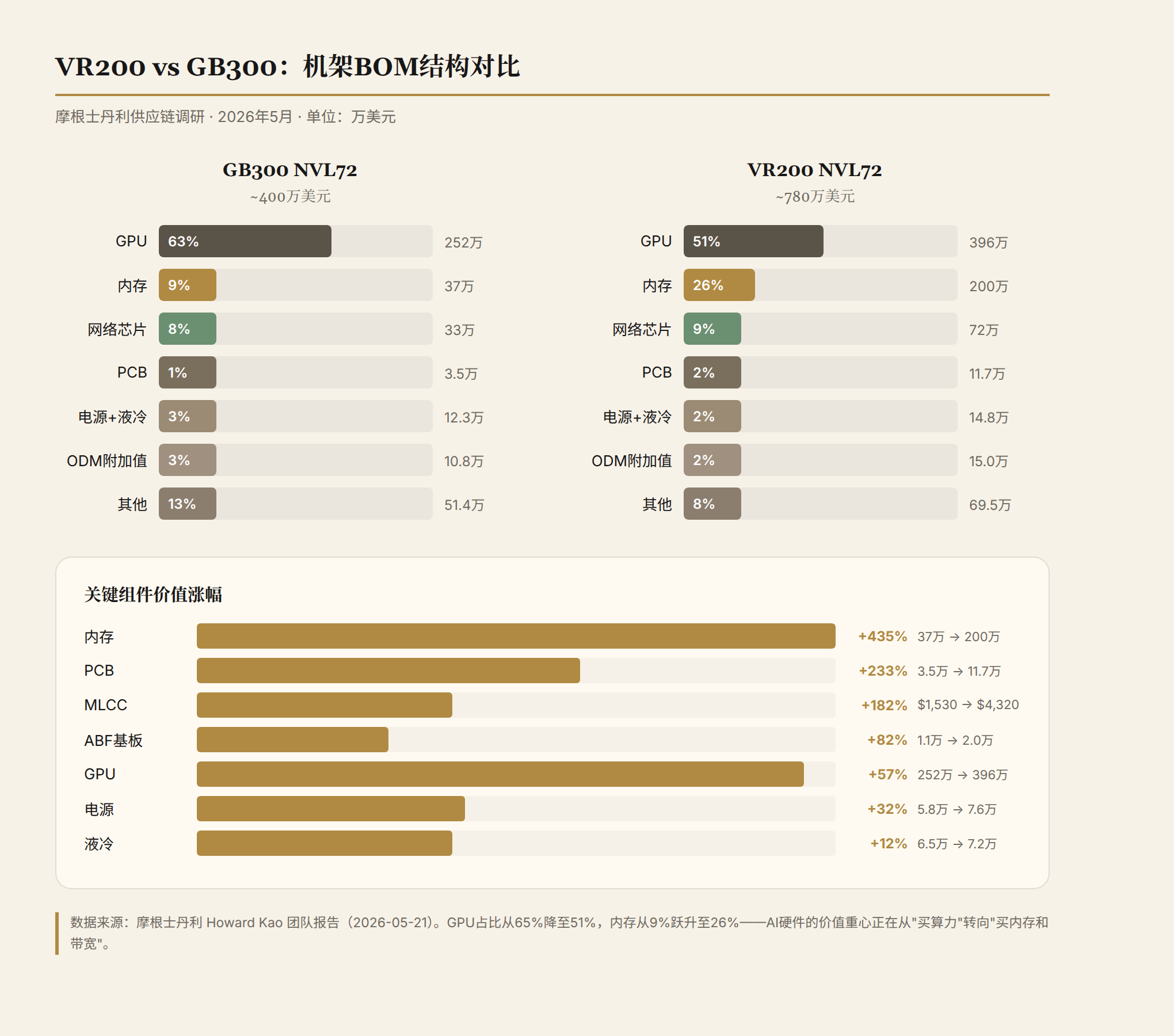

The VR200 NVL72 integrates 72 Rubin GPUs and 36 Vera CPUs, with 20.7TB HBM4 + 54TB LPDDR5X total system memory and 3.6 Exaflops peak compute. An ODM sells one of these racks for approximately $7.8 million — nearly double the ~$4M of the previous GB300.

But the real story isn't the total price — it's where the incremental value flows.

GPU remains the single largest cost item at ~$3.96M (+57% vs GB300), but its share of total BOM has dropped from 65% to 51%. Meanwhile, memory (HBM4 + LPDDR5X + 3D NAND) has surged from under 10% to 26% of total cost. PCB content is up 233%, MLCC up 182%, ABF substrate up 82%.

Nothing went down. Everything went up.

Memory: From Supporting Actor to "The New GPU"

Memory costs exploded from $370K to $2M (+435%), the single largest increment across all components. Three forces叠加:

HBM4: 72 GPUs × 288GB = 20.7TB. SK Hynix dominates supply. Estimated $400-500K.

LPDDR5X: 54TB total capacity, 3x GB200. At $8-10/GB, this alone costs $400-540K.

3D NAND: The biggest structural addition. Rubin integrates NAND flash at scale for model loading and checkpointing. Over $1M per rack, versus near-zero in GB200.

Combined, memory-related costs approach $2M — already over half the GPU cost. With NVIDIA's ~70% markup on SOCAMM memory modules, the actual economic value of memory in the system is even higher.

Key variable: If hyperscalers procure SOCAMM directly (bypassing NVIDIA's markup), rack price drops from $7.8M to ~$6.7M. That $1.1M difference is essentially NVIDIA's intermediary margin on memory.

PCB: The Largest Percentage Gainer

PCB value jumped from $35K to $117K (+233%), leading all component categories. The increment comes from three layers of stacking:

New high-value modules: ConnectX module PCBs (72 per rack × $270) and Midplane PCBs (18 × $1,500) — these didn't exist in GB300, contributing ~$46K in pure incremental value.

Existing boards upgraded across the board: Compute PCBs upgraded from 22-layer HDI to 26-layer, CCL grade from M7 to M8, unit price from $650 to $1,400. Switch PCBs from 24-layer to 32-layer. The switch upgrade is actually more aggressive than compute — interconnect complexity is growing faster than compute itself.

Physical spec improvements: Larger compute board dimensions, new 44-layer midplane PCB.

Layer count increase + material upgrade + new modules = PCB is the most elastic component in this cycle. For PCB suppliers, this is structural growth, not cyclical — AI servers don't need more boards, they need more complex and expensive ones.

MLCC and ABF: The Underappreciated Increments

MLCC surged from $1,530 to $4,320 (+182%). Murata reports a single AI server carries ~30,000 MLCCs — 30x a smartphone, 3x a car. A full NVL72 cabinet consumes 440,000 units.

ABF substrate grew from $11K to $20K (+82%). Rubin GPU ABF unit price doubled from ~$100 to $200, while NVSwitch ASICs doubled (18→36) and ConnectX chips doubled (36→72).

Power and Cooling: Forced by Power Density

Power from $58K to $76K (+32%). Underneath this modest increase is an architectural revolution: NVIDIA has confirmed 800V HVDC for the Rubin Ultra platform. Traditional 54V distribution can't handle 200kW+ per rack — the jump to 800V improves end-to-end efficiency from 87.6% to 98%.

Liquid cooling from $65K to $72K (+12%). Full liquid cooling (no fans) is now mandatory at these power densities. Including side-car CDU, total cooling reaches ~$122K.

ODM: Absolute Profits Rising, But Pricing Power Declining

ODM value-add increased from $108K to $150K (+38%) — contradicting market consensus that standardization would compress margins. System complexity increased across the board.

But gross margin declined from ~2.7% to ~1.9% as the denominator (rack price) doubled. More importantly, the consignment model is spreading — Foxconn and Quanta have both confirmed customer-direct procurement of core components, reducing ODMs to advanced assemblers.

Two Deep Signals

Signal 1: AI Hardware Costs Are Shifting from "Buying Compute" to "Buying Memory and Bandwidth"

GPU's BOM share dropped from 65% to 51%. Memory surged from 9% to 26%. If you aggregate all memory-related costs (HBM4 + LPDDR5X + NAND + SOCAMM markup), it's approaching or potentially exceeding GPU cost. This mirrors the inference bottleneck — Decode is memory-bandwidth bound, not compute bound.

Signal 2: NVIDIA's Gross Margin Peak Risk Is Real

Not from competition (there isn't any), but from three structural pressures: rising memory share (priced by others), hyperscaler direct SOCAMM procurement (bypassing NVIDIA markup), and consignment model diffusion (shifting procurement power to cloud providers).

Data Summary

| Component | GB300 | VR200 | Change | Key Driver |

|---|---|---|---|---|

| GPU | ~$2.52M | ~$3.96M | +57% | Architecture upgrade, share diluted |

| Memory (all) | ~$370K | ~$2M | +435% | HBM4 + LPDDR5X + first mass NAND |

| PCB | ~$35K | ~$117K | +233% | Layer upgrade + material + new modules |

| MLCC | ~$1,530 | ~$4,320 | +182% | Per-board usage doubled + new modules |

| ABF Substrate | ~$11K | ~$20K | +82% | GPU substrate doubled + chip count doubled |

| Power | ~$58K | ~$76K | +32% | 110kW standard + HVDC transition |

| Liquid Cooling | ~$65K | ~$72K | +12% | Full liquid + QD/manifold increase |

| ODM Value-Add | ~$108K | ~$150K | +38% | Complexity increase across the board |

| Rack Total | ~$4M | ~$7.8M | +95% | — |

Source: Morgan Stanley Research (2026-05-21), cross-validated with multiple Chinese financial media sources.

Outlook

High confidence: Storage (HBM/LPDDR/NAND) is the highest-conviction sector for the next two years. Liquid cooling has moved from optional to mandatory. Power architecture shift to 800V HVDC is a confirmed trend.

Medium confidence: PCB/CCL structural upgrade (layers + materials) drives margin expansion, not just volume. ODM short-term absolute profits rise, but long-term pricing power faces pressure from consignment.

Key variables to watch: CPO inflection timing (NVL576 may push optical engine/GPU ratio from 2-4 to 17+). HBM capacity release pace. Hyperscaler direct SOCAMM procurement progress.

Based on Morgan Stanley's Howard Kao team report "Analysis of Rubin rack BOM, component content, and ODM value-added" (2026-05-21), cross-validated with Chinese financial media.